Over the past few years, many people in the U.S. have had to deal with damage to their homes from natural disasters, such as Hurricane Harvey. This article explains the different kinds of financial protection from natural catastrophes that homeowners can access from the private and public sectors.

In 2017, Hurricane Harvey dumped over four feet of rain, flooding an area in southeastern Texas equal in size to New Jersey. One-third of Houston was underwater and over 200,000 homes were damaged. While most homeowners had insurance on their residences, typical policies did not cover damage from flooding. Homeowners in flood-prone areas have access to flood insurance provided by the government, but only 17% of those most affected by Harvey had this form of insurance. The rest had to rely on their savings, government assistance programs, and other sources to rebuild. Of the estimated $25 to $37 billion in flood damage to Texas homes resulting from Harvey, about three-quarters was uninsured.1

In this Chicago Fed Letter, we describe the types of financial protection from natural disasters, like Hurricane Harvey, that are available to homeowners from private sector providers, the federal government, and some state governments.

Private insurance

The first line of defense from financial damages caused by a natural disaster is homeowners insurance sold by commercial insurers. Most homes are covered by homeowners insurance, and this type of insurance provides good protection from some—but not all—types of damage. Homeowners insurance covers the kinds of losses that are caused by fairly localized events—typically events that do not affect a large proportion of the population in a given area at the same time. Damage to a house from a falling tree that does not affect the other houses in the neighborhood is one such example.

However, large-scale natural disasters, such as floods or earthquakes, that cause widespread damage to many homes at the same time are not typically covered by homeowners policies. The insurance treatment of such disasters has changed over time. For example, many insurance companies stopped including protection against flood damage after the 1927 Mississippi River flood led to large losses.2 Similarly, many insurance companies stopped writing earthquake insurance in California after the 1994 Northridge earthquake. From the insurance companies’ standpoint, it makes sense to charge customers additional premiums for such coverage—it is difficult to predict losses from such events, and insurers may have to pay out large sums in a fairly short period, requiring them to hold extra capital.

According to recent reports, private insurance policies with specific protections from natural disasters are mainly purchased to protect high-value homes and tend to be expensive, likely limiting their appeal. Thus, even in flood- and earthquake-prone areas of the country, take-up rates are low.3

Government programs

The government has assumed an active role in providing financial protection against natural-disaster-related risks left out of privately provided insurance policies. After private insurers largely stopped offering protection against damage due to massive floods in the 1920s, the government found itself providing relief for flood victims on an ad hoc basis—paid for out of the general budget. The government also sometimes stepped in after other kinds of disasters, such as earthquakes. But it was not always clear whether there would be government aid or which level of government (local, state, or federal) would provide this aid. Moreover, the response could be piecemeal and uncoordinated. After Hurricane Betsy hit several southern states in 1965, President Lyndon Johnson called on different parts of the government to provide aid to stricken areas.4 But this aid was expensive. In response to these high costs, the National Flood Insurance Act of 1968 was passed. This act led to the creation of the National Flood Insurance Program (NFIP), which mandated the purchase of flood insurance for homeowners with a federally backed mortgage residing in flood-prone areas.5 Making flood insurance mandatory passed some of the burden for disaster recovery from the government (ultimately, all taxpayers) to exposed homeowners.

Heading into the late 1970s, the governmental response to natural disasters (often involving multiple federal agencies and state and local governments) was still fragmented. While not a natural disaster, the Three Mile Island nuclear plant meltdown in 1979 illustrated the difficulty of a quick and coordinated governmental response to a disaster. That same year President Jimmy Carter established the Federal Emergency Management Agency (FEMA) to coordinate the federal government’s response, and the NFIP was placed under the aegis of FEMA. Over time, changes have been made to FEMA and to the laws governing federal disaster relief to address perceived weaknesses in FEMA’s response to declared disasters.6

National Flood Insurance Program

Government-backed insurance programs, such as the NFIP, provide a second line of defense against losses from natural disasters. The NFIP protects policyholders from damages caused by flooding. The idea behind the NFIP was to shift some of the costs of flooding to developers and homeowners. This would reduce the cost to taxpayers and might get developers to pay more attention to flood risk when deciding where to build. Initially, risk under the NFIP was shared by private insurers, but eventually the government took on all the insurance risk.7

The Flood Disaster Protection Act of 1973 required the NFIP to identify flood-prone communities and categorize them by probability and potential severity of flooding. Regions that are 100-year floodplains (those calculated to have a 1% chance of being inundated by a flood in a year) are called Special Flood Hazard Areas (SFHAs).8 Homeowners in these regions are required to purchase flood insurance if they have a mortgage from a federally regulated lending institution; have a mortgage guaranteed by Fannie Mae, Freddie Mac, or Ginnie Mae;9 or have received federal disaster assistance for their flood-damaged homes.10 In addition, people who live in communities that demonstrate to the NFIP that they are taking steps to minimize flood damage can become eligible to purchase federal flood insurance.11

The NFIP offers most homeowners exposed to flood risk an avenue to get insurance, but the take-up rate is low. As noted earlier, it is estimated that only 17% of those most affected by Harvey had flood insurance. Similarly, it was found that among those most affected by Hurricane Sandy in 2012, less than 20% had flood insurance.12 Broader data on flood insurance usage are consistent with these findings. According to a RAND Corporation estimate, within the 100-year floodplains, the market penetration rate of residential flood insurance among single-family homes is about 50%, but outside of those areas, it is about 1%; overall, about 3% of single-family homes have federal flood insurance.13 Flood insurance policies are concentrated in the states bordering the Gulf of Mexico. According to our analysis of FEMA data, Florida, Louisiana, and Texas combine for over half of flood insurance premiums, and Florida and Louisiana have by far the highest premiums paid per capita.

California Earthquake Authority

Earthquakes, while less frequent than hurricanes, can cause larger losses. Of the 40 costliest insurance losses since 1970, the earthquake category (made up of seven earthquakes) had a higher average economic loss than any other kind of natural disaster category.14 One of these earthquakes was the Northridge earthquake of January 1994.

Into the 1990s, insurers were required to include coverage for earthquake damage in homeowners insurance policies in California. After the Northridge earthquake, the vast majority of insurers indicated they would rather not write any insurance if they had to offer earthquake protection. By January 1995, companies representing 93% of the California homeowners insurance market had either restricted homeowners policies or ceased writing them altogether. Eventually, California permitted policies without earthquake protection. Because this left residents potentially exposed, in 1996 California created the California Earthquake Authority (CEA)—a publicly managed, privately funded nonprofit organization. The CEA offers earthquake insurance for California homeowners (and renters). State law requires that CEA earthquake insurance policies have actuarially sound rates—rates at which the full expected cost of insuring risk for earthquake damage is recouped. Homeowners can purchase insurance on the full value of their home minus a deductible. As of 2015, about 10% of California homeowners had earthquake insurance through the CEA.15

Disaster declarations

When the President issues a presidential disaster declaration, FEMA can step in to provide direct assistance to homeowners and others through the Disaster Relief Fund. In addition, the Small Business Administration (SBA) can offer (subsidized) disaster loans to households (and businesses).16

FEMA distributes funding to the areas where a disaster has been declared through three primary channels: public assistance (general cleanup and repair), individual assistance (emergency housing and care), and hazard mitigation. The exact form of the federal disaster relief depends on the specific scenario. FEMA can offer an individual household as much as $34,000 in an emergency grant, but generally direct grants to households are substantially smaller.17

For fiscal year 2017, Congress appropriated $7.3 billion for FEMA’s base disaster relief budget. Base funding has increased in recent years. Congress generally appropriated $1 to $2 billion in base funding in the 2000s, while it set aside $100 to $300 million in base funding in the 1990s. If a situation requires funding that would outstrip FEMA’s base disaster relief budget, which generally happens at least once per year, Congress may direct supplemental appropriations to disaster relief. According to a report from the Congressional Research Service, Congress did so 14 times between 2004 and 2013, for a total of $89.6 billion in additional funding.18

Homeowners can also get relief through SBA loans once there has been an official presidential disaster declaration. The total size of SBA disaster loans is large relative to FEMA aid. For example, after Hurricane Sandy, the SBA provided $2.5 billion in loans, compared with $250 million in NFIP payments from FEMA.19 Yet funds from the SBA need to be repaid eventually, unlike those from FEMA.

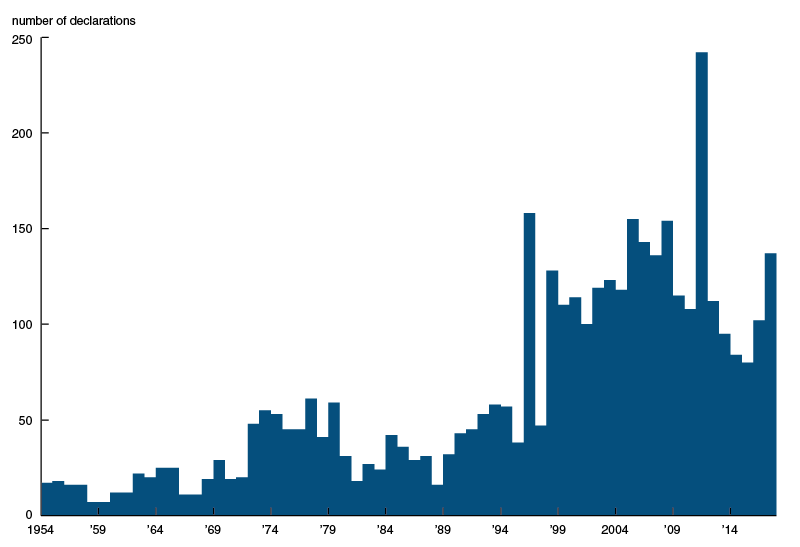

Since the federal disaster declaration program began in the 1950s, the number of disaster declarations per year has increased substantially, from generally under 25 per year in the 1950s to generally over 100 per year since the late 1990s (see figure 1). In total, there have been almost 4,000 declarations since the 1950s, about two-thirds of which have occurred since 1996.

1. Disaster declarations, 1954–2017

The role of the federal government in disaster relief has increased substantially over time, especially after 2000. For example, experts estimate that the share of hurricane-related losses that the federal government covered was about one-quarter before Hurricane Katrina in 2005, but jumped to over two-thirds for Hurricane Katrina and subsequent large hurricanes.20 Much of the federal aid went to state and local governments, rather than directly to individual households.

Summary

Natural disasters can have deep and lasting effects. For example, one year after Hurricane Harvey, 30% of Texans affected by the storm stated that their lives were still not back to normal.21 Much of the damage to homes caused by Harvey was not covered by private homeowners insurance. The government has historically stepped in by providing insurance and direct relief to communities hard hit by natural disasters. Insurance and assistance provided by the government fills in some of the gap left by private insurance. One federal program, the National Flood Insurance Program, offers insurance against flood damage for homes in flood-prone areas. One issue (as seen in Texas following Harvey) is that not all eligible homeowners purchased insurance under the NFIP. States can also act to protect their citizens with programs like the California Earthquake Authority, but low insurance take-up rates under such programs can be an issue as well.

In addition to insurance programs, the government can provide other aid to communities when an official disaster declaration has been made by the President. FEMA offers small grants to tide households over. And the SBA can offer loans to help them rebuild their homes.

In this article, we have sought to clarify the roles of private insurance and government programs in protecting households and communities against the devastating losses that can arise from natural catastrophes.

1 All the information related to Harvey in this paragraph is from a November 2018 Balance article; an August 2017 Washington Post Wonkblog entry; and a January 2018 CoreLogic press release.

3 See, e.g., this June 2010 Wall Street Journal article, available online by subscription; the Insurance Information Institute’s Facts + Statistics: Flood Insurance webpage; and this February 2018 Seattle Times article.

5 The Flood Disaster Protection Act of 1973 (which amended the National Flood Insurance Act of 1968) made the purchase of flood insurance mandatory for such homeowners.

6 More on FEMA’s history is available online.

11 For more information, see the NFIP’s FAQs. Flood insurance under the NFIP covers losses up to a limit of $250,000 for a dwelling and $100,000 for personal property; these and further details are available online.

15 Some details in this paragraph are from the CEA’s own history webpage. Additional information is from a February 2017 Resources for the Future issue brief. There is some private earthquake insurance in California. It is more expensive than insurance from the CEA. In 2016, about 80% of California earthquake insurance policies were CEA policies; and roughly 75% of the premiums from California earthquake policies were for CEA policies, according to a California Department of Insurance report.

16 Additionally, the U.S. Department of Agriculture has multiple programs to financially assist farmers recover from natural-disaster-related losses; details are available online.

17 This information is from a June 2018 CRS (Congressional Research Service) Report for Congress, available online, and a September 2017 Reuters story.

18 All the FEMA-related information in this paragraph is from the Consolidated Appropriations Act, 2017, Pub. L. No. 115-31, Division F, Title III, available online, and a May 2014 CRS Report for Congress, available online.

19 The SBA loans value is from a September 2017 CNBC story; the FEMA payments value is from a June 2017 FEMA fact sheet.