The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

The Midwest has a long-standing reputation as an ugly duckling during national economic slowdowns.1 This reputation was acquired and richly deserved as a result of the region’s performance in the 1970, 1973-75, 1980, and 1981-82 recessions. During these episodes manufacturing activity, housing, retail sales, and employment all posted sharply greater declines in the Midwest than the national average.

Early this year, hints of slowing growth in interest-rate-sensitive industries raised questions in some quarters about the Midwest’s ability to sustain the high rates of growth established in 1994. Given historical patterns, it might have seemed reasonable to look to the Midwest for an early signal of any change in national economic performance.

But is the Midwest economy still the ugly duckling? If the region always suffers worse than the nation during periods of economic slowing, why did the gap between the Midwest and U.S. unemployment rates continue to move in the region’s favor from 1989 to 1991? Why did the region’s share of U.S. employment continue to rise over these years, despite a long-run trend of faster population growth in the nation as a whole, and despite the fact that the region has a higher share of cyclically sensitive manufacturing employment than the national average?

Midwest economic activity has continued to outperform the national average in recent years, with particularly vigorous gains in 1994. Has the region transformed itself from an ugly duckling to a swan? This Fed Letter will examine the performance of the Midwest economy in 1994, placing it in the context of a remarkable regional turnabout.

Demand for Midwest workers strengthens further

The Midwest economy generated jobs at a faster rate in 1994 than in 1993, and many indicators depict tighter labor markets in the Midwest than the nation.2 Payroll survey employment estimates for 1993 and 1994 were recently revised upward during the annual benchmarking process. This region’s employment is now estimated to have increased 2.2% in 1993 and 3% in 1994, up from the 1.7% and 2.1% originally estimated for those years, respectively. The revised data still suggest that employment grew slightly more rapidly in the Midwest in 1994 than in the nation, as it has every year since 1986. The Midwest’s slowly increasing employment share over this period has not yet proven strong enough to erase the picture of a longer-term downtrend, however, primarily because of faster population growth in the South and West. Nonetheless, the payroll survey data suggest that the Midwest has now posted nine consecutive years of greater employment growth than the national average, easily the longest such streak since World War II.

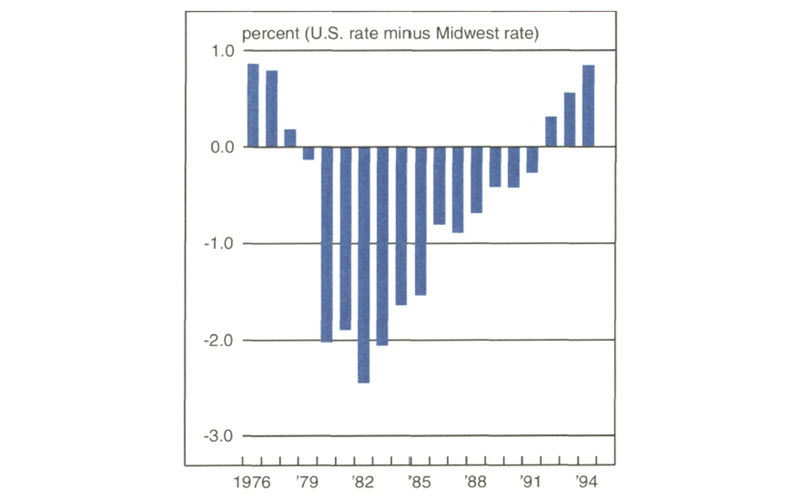

Unemployment rates provide an alternative indicator for comparing longer-term changes in welfare and job opportunities (on a per capita basis) across regions, as they can control for the impact of population growth. The aggregate unemployment rate for the Midwest states fell from 6.3% in 1993 to 5.2% in 1994. These figures may actually understate the degree of improvement, as new survey methods probably showed a higher rate in 1994 than the earlier method. The Midwest unemployment rate continued to decline within 1994, falling by year-end to the lowest level since at least 1977. Nationally, the unemployment rate averaged 6.1% in 1994, and the gap between the Midwest and U.S. rates widened further in the region’s favor (see figure 1). Previous recessions had a clearly concentrated impact on labor markets in this region, and the Midwest unemployment rate climbed fully 2.5 percentage points above the national average in 1982. Since then, however, the gap between the Midwest and the U.S. rates has consistently trended in the Midwest’s favor, even in the recessionary years of 1990 and 1991.

1. Relative unemployment rate

Privately produced labor market indicators continued to depict relatively strong employment gains in the region. For example, Manpower’s hiring plans survey showed that the net percentage of Midwest employers planning to add workers rose from 15% in 1993 to 20% in 1994, remaining above its national counterpart for the sixth consecutive year. (This survey produces a diffusion index, and an increase in the index is consistent not simply with increased employment, but with increased employment growth.) Trends in help-wanted advertising also pointed to a substantial increase in the demand for labor in the Midwest during 1994. According to the Conference Board survey, recruitment advertising continued to increase at a faster pace in the East North Central census region than the national average. Advertising initially responded sluggishly to the recovery from the 1990-91 recession, as employers first used word-of-mouth and other less costly forms of recruitment while expanding their labor force. As the supply of readily available workers grew increasingly lean in 1993 and 1994, however, help-wanted advertising and similar forms of recruitment gained greater strength. If help-wanted ads are a good leading indicator going into a slowdown (as they were in 1989 and 1990), recent developments do not point to any near-term slowing. Recruitment advertising surged in the final quarter of 1994, both nationally and in the Midwest.

Some of the most difficult issues involved in estimating economic statistics lie in measuring the aggregate contribution of activity generated by small firms. In this regard, the National Federation of Independent Business (NFIB) provides an ongoing measure of current business conditions, future spending plans, and general expectations. The NFIB overall “optimism index” for the Midwest has been moving in line with its national counterpart in recent years, but the component called “job openings you cannot fill” accounted for a substantial share of the overall increase, rising sharply in 1993 and 1994.

Labor market strengthening finally showed some headway in the Conference Board’s survey of consumer confidence during 1994. The East North Central census region recently posted the highest overall index (along with the Mountain states) among the nine census regions. It also showed the greatest improvement (along with the Pacific states) over the past year. According to this survey, consumers’ appraisals of job opportunities remained relatively depressed in 1992 and 1993, even as employment growth gained greater momentum. Continuing, highly visible layoff announcements by large firms contributed to the general apprehension. Job cutback announcements fell considerably by early 1995, however, according to a study by an outplacement consulting firm. Another recent survey showed that hiring plans for the relatively hard-hit middle manager class climbed to their highest levels since 1984, with the North Central region showing the strongest conditions. In turn, the consumer confidence survey showed that appraisals of Midwest labor markets have strengthened considerably over the past year.

Region’s success due to factors within and without

National economic patterns provided a favorable backdrop for Midwest growth in recent years, while production in the region seems to have gained share of national output in several important sectors. Nationally, real GDP increased at a faster pace in 1994 than in 1993, partly because recoveries gathered greater momentum in several regions that had previously lagged the national average. Their tardy but welcome expansion helped to reinforce growth in demand for goods produced in the Midwest.

The composition of national economic growth by spending category also remained favorable from a Midwest perspective. Real personal spending on durable goods rose 9% in 1994, in line with its increase in 1993 and more than twice the rate of overall GDP growth. Similarly, real business investment on producers’ durable equipment rose 18%, in line with its gain in 1993 and about four times the rate of GDP growth. Merchandise exports rose 11% in 1994, more than twice as fast as in 1993 and about twice as fast as overall GDP. These spending categories are especially important to the Midwest, as manufacturing production in these categories yields a disproportionate share of personal income in the region.

Midwest manufacturing activity closed out 1994 on a high note and generally remained vigorous in early 1995. Purchasing managers’ surveys provide timely and comprehensive insights into regional manufacturing trends, and surveys are conducted in Chicago, Detroit, Milwaukee, and western Michigan. The composite production component of these surveys pointed to accelerating output growth (and faster growth than the national average) from 1992 to 1994. In turn, payroll data suggest that Midwest manufacturing employment posted its largest annual increase in 1994 since 1977, while the region’s share of U.S. manufacturing employment climbed at an accelerating pace over the past three years.

Payroll survey data suggest that national manufacturing employment showed little if any recovery from the 1990-91 recession until the latter half of 1994. However, the growing use of temporary workers in manufacturing occupations, efforts to place employment more accurately at the establishment level, and related industry code reclassifications may have significantly affected estimates of “manufacturing” employment (as well as unit labor costs and productivity) in recent years. Interestingly, Manpower’s survey suggests that manufacturers’ hiring plans actually posted a stronger recovery than those of other employers in 1992, 1993, and 1994, both nationally and regionally. The Manpower survey has also shown that hiring plans among midwestern manufacturers have been significantly stronger than their national counterparts since 1990. Purchasing managers’ surveys also pointed to faster growth in Midwest manufacturing employment in 1994 than in 1993 and continued faster growth than the national average.

The Midwest continued to gain share of output in 1994 in motor vehicle assemblies. Nationally, the production of motor vehicles and parts increased at roughly the same pace in 1994 as in 1993, and about twice as fast as overall manufacturing output. We lack a good measure of parts output for the region, but light vehicle assemblies in the Midwest increased twice as fast in 1994 as they did in 1993, and almost twice as fast as the national average. In sharp contrast to the early 1980s’ recessions, the region’s share of U.S. car and light truck assemblies climbed relatively strongly in the late 1980s, through the 1990-91 recession, and on into the early 1990s. Rising output in Canada and Mexico do not help account for the increase in the Midwest’s share of national assemblies, as the Midwest’s share of North American assemblies has posted similar gains in recent years.

The growing competitiveness of Midwest manufacturers in international markets has been a much-discussed but difficult-to-pin-down source of strength for the region. State-level export data suffer from a variety of delicate and perhaps intractable estimation challenges.3 The latest available Commerce Department data suggest, however, that in 1994, export shipments from manufacturers in the Midwest grew three times as fast as those of their national counterparts.

Improvement in employment opportunities and personal income continued to boost housing activity and supporting industries in the region during 1994, although housing activity moderated in late 1994 and early 1995. Housing starts grew more rapidly in the Midwest in 1994 than in 1993, reaching their highest annualized level since 1979. From this longer-term perspective, housing starts provide some of the most dramatic evidence of the turnabout in the relative performance of the region’s economy. From 1976 to 1983, the Midwest’s share of national single-family housing starts was steadily cut in half (from 26% to 13%), but it gained back nearly all the lost ground by 1992, climbing to 24% in spite of faster population growth in the nation as a whole. The Midwest’s share did decline slightly in 1993 and 1994, however, as recoveries gathered greater momentum in other previously weak regions. Existing single-family home sales in the region also grew faster than the national average from 1989 to 1992, but then slightly underperformed the nation in 1993 and 1994. A slowdown in home sales in the second half of 1994 was far more evident in the national data than in the Midwest, however.

Are we this good, or just this lucky?

The Midwest economy outperformed the national average in 1994, as it often does when the national economy is doing well. Over the past few years, however, the region seems to have profited from productivity improvement and an increased share of national output in cyclically sensitive industries. This helps explain why the Midwest’s legendary and still-feared sensitivity to national slowdowns failed to materialize in 1990 and 1991. The region certainly did not escape the most recent recession, but the improved competitiveness of Midwest producers stood the region in good stead. In turn, improved productivity helped the region make the most of its concentration in cyclically sensitive industries during 1992, 1993, and 1994.

The Midwest economy has also benefited from a set of fortunate external conditions since the early 1980s, however, including declining long-term interest rates, an increasingly favorable environment for international trade, and, perhaps most important, the fact that energy prices have declined to some of their lowest levels (in real terms) in the past three decades. Under these conditions, the Midwest’s prospects for growth in 1995 remain bright.

Tracking Midwest manufacturing activity

Manufacturing output indexes (1987=100)

| January | Month ago | Year ago | |

| MMI | 142.5 | 141.4 | 128.9 |

| IP | 124.2 | 123.8 | 115.8 |

Motor vehicle production (millions, seasonally adj. annual rate)

| January | Month ago | Year ago | |

| Autos | 7.2 | 7.0 | 6.9 |

| Light trucks | 5.5 | 5.6 | 5.2 |

Purchasing managers’ surveys: net % reporting production growth

| February | Month ago | Year ago | |

| MW | 67.3 | 69.4 | 72.2 |

| U.S. | 54.8 | 62.7 | 58.7 |

Purchasing managers’ surveys (production index)

Sources: The Midwest Manufacturing Index (MMI) is a composite index of 15 industries based on monthly hours worked and kilowatt hours. IP represents the Federal Reserve Board industrial production index for the U.S. manufacturing sector. Autos and light trucks are measured in annualized units, using seasonal adjustments developed by the Board. The purchasing managers’ survey data for the Midwest are weighted averages of the seasonally adjusted production components from the Chicago, Detroit, and Milwaukee Purchasing Managers’ Association surveys, with assistance from Bishop Associates, Comerica, and the University of Wisconsin-Milwaukee.

Midwest manufacturing activity continued to expand at a moderate to vigorous pace in recent months. The composite index of production components in purchasing managers’ surveys for Chicago, Detroit, and Milwaukee showed continued robust expansion in output, in contrast to the slower growth indicated in the national data.

Automakers’ plans currently call for a slight decline in assemblies in the second quarter. If targets are achieved, however, assemblies would still reach one of their highest quarterly output levels in the past eight years.

Notes

1 See “Slowdown will hit regions differently,” Wall Street Journal, February 24, 1995, page A2.

2 Unless otherwise specified, “Midwest” refers to Illinois, Indiana, Iowa, Wisconsin, and Michigan.

3 Cletus C. Coughlin and Thomas B. Mandelbaum, “Measuring state exports: Is there a better way?” Review, Federal Reserve Bank of St. Louis, Vol. 73, No. 4, July/August 1991, pp. 65-79.