The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

In 1997, the economy expanded with gusto in the first quarter, rising by nearly 5%, and then moderated in the second and third quarters, gaining 3.3% and 3.5%, respectively. Observers feared that such high growth was unsustainable without causing the economy to overheat and inflation to rise. However, the year witnessed a downward trend in both the unemployment rate and inflation. Still, the lag structure between strong economic growth and inflation is not clearly defined, and concern about inflation remained even as the inflation rate dipped below 2%, its lowest level in over ten years. The Asian economic crisis in October led to increased stock market volatility, strengthened the dollar, and added a new wrinkle to the U.S. economic horizon.

Against this backdrop, the Federal Reserve Bank of Chicago held its 11th annual Economic Outlook Symposium on December 5, 1997. More than 50 economists and analysts from business, academia, and government attended the conference. The focus of this year’s conference was on the labor market and whether an economy operating at full employment can continue to expand when it is running out of workers. This Fed Letter reviews the accuracy of last year’s conference forecasts and summarizes the 1998 Economic Outlook Symposium.

Looking over our shoulders

Generally, participants in last year’s symposium underestimated the strength of the economy. They expected real gross domestic product (GDP) to increase by just over 2% in 1997; for the first three quarters, it averaged just under 4%. This underestimation tendency held for most of the subcategories of GDP. The 5.2% growth rate of industrial production for the first three quarters of 1997 was more than twice the forecast. Light vehicle sales averaged 406,000 more units than forecast a year ago. Housing starts were expected to moderate to 1.39 million units in 1997 after a very strong year in 1996; instead, 1.46 million annualized units were added in the first three quarters. The trade-weighted dollar was anticipated to increase a slight 0.9% during 1997; however, the dollar appreciated nearly 17% for the year. An overestimation of 0.4 percentage points occurred for the unemployment rate forecast. The inflation rate was expected to soften in 1997 to a 2.8% rate, following the 2.9% average of 1996. However, it ended half a percentage point lower than the forecast at 2.3%.

The symposium forecast was more accurate on interest rates, with the actual rate being only 28 basis points higher than the forecast for 1997.

In summary, the economy expanded faster, inflation was more benign, and unemployment rates were lower than last year’s symposium forecasts suggested. With unemployment rates now below 5%, and in many regions under 4%, businesses are increasingly becoming concerned about finding qualified workers. This concern raised the question that became the theme of the 1998 Economic Outlook Symposium, “Where have all the workers gone?”

Looking ahead

For 1998, the symposium forecasts show the positive 1997 economic conditions continuing, albeit at a much slower pace. Figure 1 summarizes expectations for 1997 (fourth quarter numbers not known) and 1998. Most forecasters believed that the growth rates experienced in 1997 are unsustainable and that real output growth during 1998 will be lower than in 1997 for every subcategory of GDP. The typical forecaster is expecting real GDP growth to be 3.8% in 1997 and 2.6% in 1998. Given the situation in Asia, it is not surprising that one of most dramatic changes anticipated during 1998 is on the international front, with net exports forecast to decline from –$145.4 billion in 1997 to –$176 billion in 1998. Only the government sector is expected to grow in 1998 at rates similar to 1997.

1. Median forecasts from the 1998 Economic Outlook Symposium

| 1996 | 1997 | 1998 | |

| Real GDP | 2.8% | 3.8% | 2.6% |

| Personal consumption expenditures | 2.6% | 3.3% | 3.0% |

| Business fixed investment | 9.2% | 10.6% | 9.2% |

| Residential construction | 5.9% | 2.3% | 2.1% |

| Change in business inventories (bil. constant $) | $25.0 | $60.5 | $38.5 |

| Net exports of goods and services (bil. constant $) | –$114.4 | –$145.4 | –$176.0 |

| Government purchases of goods and services | 0.5% | 1.0% | 1.1% |

| Industrial production | 2.8% | 4.6% | 3.5% |

| Car and light truck sales (millions) | 15.0 | 15.0 | 14.8 |

| Housing starts (millions) | 1.47 | 1.46 | 1.41 |

| Unemployment rate | 5.4% | 5.0% | 4.9% |

| Inflation rate (Consumer Price Index) | 2.9% | 2.4% | 2.4% |

| Prime rate | 8.27% | 8.44% | 8.70% |

| Federal Reserve trade-weighted dollar | 3.6% | 10.5% | 1.0% |

Sources: U.S. Bureau of Economic Analysis; Federal Reserve Board of Governors, various releases; U.S. Department of Commerce, Bureau of the Census; U.S. Department of Labor, Monthly Labor Review, various years; U.S. Department of Labor, Bureau of Labor Statistics; and Federal Reserve Bank of Chicago, Economic Outlook Symposium.

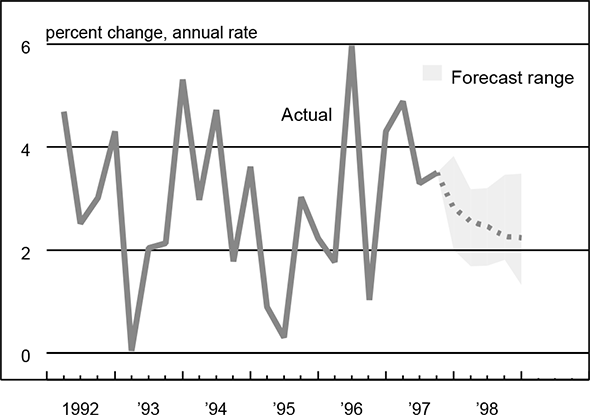

In terms of the quarterly pattern for real GDP, the forecast group is expecting a downward trend. In the first quarter, real GDP growth is forecast at 2.8%, moderating steadily to 2.2% by the fourth quarter of 1998 (see figure 2). This downward pattern is reflected in the growth outlook for personal consumption expenditures, business fixed investment, and residential investment. Some weakening is expected for change in business inventories and net exports. Government spending growth is forecast to remain fairly flat over the four quarters of 1998.

2. Real GDP growth

Source: U.S. Bureau of Economic Analysis.

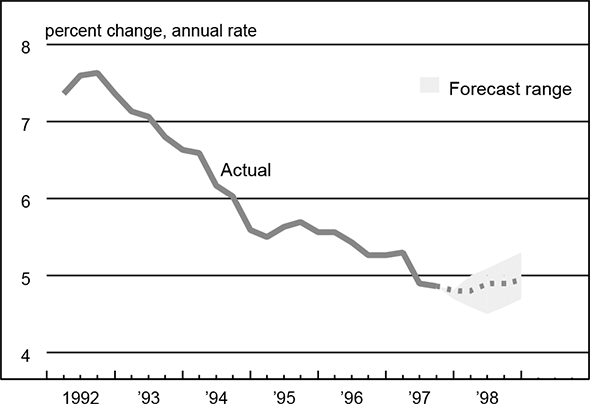

The quarterly patterns for the other series forecasts—industrial production growth, car and light truck sales, and housing starts—are expected to decline over the forecast horizon. The unemployment rate (see figure 3), inflation, and the prime rate are anticipated to rise over the four quarters of 1998. Finally, the growth rate for the trade-weighted dollar should show a fairly flat pattern in 1998. Below, we summarize the discussion of tight labor markets and forecasts for individual sectors.

3. Change in unemployment rate

Source: U.S. Department of Labor, Bureau of Labor Statistics.

Dealing with tight labor markets

A chief executive officer (CEO) from a temporary help firm said that while jobs are being created at a fast pace, there are major discrepancies between jobs and individuals available to fill them, both in terms of geography and education.

The speaker proposed several solutions to the tight labor force problem: 1) Outsourcing of positions to temporary help agencies to reduce the cost of mis-hiring, one of the more significant costs that companies incur. 2) Training of employees to keep their skills current. Corporate training has been one of the areas most affected by cost cutting. 3) Bringing retirees back into the work force. 4) Using expanded hiring sources, such as the Internet, networking through new hires, looking at individuals just out of high school who are not sure what job they want to hold, or creating alliances with correspondence schools. 5) Reducing turnover through a combination of nonmonetary and monetary incentives. 6) Preparing students better for the working world. Finally, the speaker asked whether, in a full employment environment, currently unemployed individuals are in fact employable. Do they even have basic job skills? What can be done about this portion of the unemployment group?

According to the CEO, the labor markets will continue to be very tight and the gap will persist between what employers want and what is available.

Outlook for individual sectors

Consumer

The economic outlook from the consumer side was discussed by an economist who has worked with consumer surveys extensively for many years. Consumers typically decide to stop spending only if some major economic or political event changes the economic horizon and, at this time, they generally expect the current expansion to last another five years. The consumer has not been this optimistic about conditions since 1965. Indicative that consumers expect low rates of inflation to continue is that the inflationary mentality that they should buy now before prices go up no longer exists. There does not appear to be any significant pent-up demand, so consumers now feel they can shop elsewhere if prices are high. This view has placed increased competitive pressures on some producers, making it difficult to pass on higher manufacturing costs to consumers. Based on the surveys, consumers are not as concerned about becoming unemployed as they were a short time ago

Autos

An economist from an auto producer expects light vehicle sales (seasonally adjusted annual rate) to be 14.7 million to 15.2 million units, which is in the range of the consensus forecast of 14.8 million units. This economist felt that there does not appear to be a large amount of pent-up demand. Feeling confident about the economy, consumers have continued to make large purchases, such as vehicles, in the past year. The economist expects core inflation to be under 2% in 1998 and interest rates to be stable, which should lead to good retail sales and vehicle sales. The risks to domestic vehicle producer sales are continued competition from European producers and increased competition from Asian producers, in particular Japan and South Korea. Having lost sales in the Far East due to the Asian economic crisis, Japan and South Korea will probably try to ship more product to the U.S. to keep their production levels up. This increased competition will lead to even lower vehicle prices for consumers in 1998. With reduced production and consumption demand in Asia, this economist expects crude oil prices to be down by 20% in 1998. This is good news for light truck sales, as these vehicles tend to be less fuel efficient than passenger cars.

Home building

An executive who represents the home building industry presented a very favorable outlook for the housing industry in 1998. Competition has increased for home builders, with more builders competing for market share. It has been quite a buyers’ market, with incentives being offered by builders. Builders are not having trouble finding labor, and wages have not increased significantly over the past year. With the strong sales pace of the past several years, there does not appear to be any pent-up demand in the housing market. This executive expects housing starts to ease to 1.39 million units in 1998. The consensus forecast for 1998 is slightly more optimistic at 1.41 million units.

Steel

A consultant to the steel industry said that many major projects will be undertaken in 1998 and that given the amount of steel being shipped, the construction numbers being reported are too low. Steel consumption is projected to increase nearly 2% in 1998. Engine and parts plants and assembly plants in the automotive industry are the most active sectors for investment in this industry. There do not appear to be any capacity constraints, with the possible exception of high-performance products. Compensation is generally high in the steel industry, making it relatively easy to attract workers. Furthermore, the consultant felt that wages in this industry do not accurately represent the total compensation that employees receive. Front-end or performance-based bonuses, as well as profit-sharing plans, add to total compensation.

Banking

The concern over rising consumer credit card debt was discussed by an economist from a large commercial bank. Despite improving economic conditions, debt levels have increased to record levels. However, the speaker felt that consumers are getting smarter about managing debt. More aggressive credit card marketing by issuers explains part of the debt buildup. In addition, consumers are feeling more confident and are more willing to extend their credit obligations.

In 1998, the banking industry faces some challenges. While short-term interest rates have remained fairly steady, long-term interest rates have come down since the middle of 1997, leading to a flattening of the yield curve. This will hurt the profit margins of banks, which make their money by borrowing short and lending long. Consolidation in the banking industry will continue. There are 25% fewer banks in the U.S. now than in 1990.

Heavy equipment

According to a director of the economics department of a heavy equipment manufacturer, the industry is heavily reliant on how well the construction industry does during 1998. The industry is currently in an upsurge. While tightness in the labor market continues to be a concern, this industry has been less affected than other industries. Productivity gains have allowed the speaker’s company to reduce employment, while increasing both sales and shipments. For new hires at this company, there were 25 applicants for every opening and, of those hired, more than 70% had college degrees. The North American market for heavy duty equipment is very mature and any expansion in this market in 1998 and beyond will be from foreign demand. The environment for machine sales for both the agriculture and construction industries during 1998 is very favorable. The heavy equipment industry does well as long as housing starts remain above a 1.3 million unit pace. As long as the economy doesn’t go into a recession and as long as interest rates remain somewhat stable, the speaker believes that the outlook for the industry will remain bright.

Conclusion

The economic outlook for 1998 calls for slower economic growth than in 1997, coupled with a continued low rate of inflation and a low unemployment rate. Both light vehicle sales and housing starts are anticipated to be down slightly from their 1997 levels, but still at fairly high rates. If these forecasts are realized, 1998 will be another in a series of very good years for the U.S. economy.

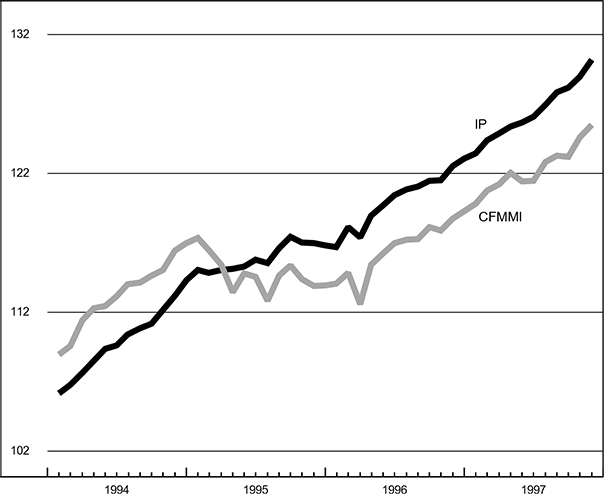

Tracking Midwest manufacturing activity

Manufacturing output indexes (1992=100)

| November | Month ago | Year ago | |

|---|---|---|---|

| CFMMI | 125.5 | 124.6 | 118.8 |

| IP | 130.2 | 129.0 | 122.5 |

Motor vehicle production (millions, seasonally adj. annual rate)

| November | Month ago | Year ago | |

|---|---|---|---|

| Cars | 6.1 | 5.9 | 6.3 |

| Light trucks | 6.6 | 6.2 | 5.6 |

Purchasing managers’ surveys: net % reporting production growth

| December | Month ago | Year ago | |

|---|---|---|---|

| MW | 58.6 | 63.7 | 58.4 |

| U.S. | 55.4 | 58.6 | 58.5 |

Manufacturing output indexes, 1992=100

The CFMMI reached a record high of 125.5 in November. The index gained 0.7% for the month, following a strong 1.1% increase in October. The Federal Reserve Board’s IP for manufacturing also set a record high of 130.2 in November, gaining 1% for the month following a 0.6% increase in October.

The Midwest purchasing managers’ composite index for production decreased to 58.6% in December from 63.7% in November. Purchasing managers’ indexes decreased for the Chicago, Detroit, and Milwaukee surveys. The national purchasing managers’ composite index decreased from 58.6% in November to 55.4% in December. Total motor vehicle production increased from 12.1 million units in October to 12.7 million units in November. Light truck production increased from 6.2 million to 6.6 million units and car production increased from 5.9 million to 6.1 million units.