The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

A recent study of retail industries near the U.S.–Canada border measures how quickly new competition arrives after an increase in demand.

In this Chicago Fed Letter, we describe our recent research on the effects of real exchange rates on the number of producers and their average employment in U.S. retail trade industries located near the U.S.–Canada border.1 Our results yield new measures of the speed with which new producers enter retail trade industries following demand shocks. Microeconomic theory assumes that the number of producers is fixed immediately after an increase in demand and that potential entrants can only take advantage of the resulting profit opportunity with the passage of time. Our estimates of the speed of entry quantify the time required for this transition from the short run to the long run. In three of the four industries we examine, this time is at most one year. Thus, changes in the number of producers contribute to these industries’ cyclical fluctuations.

There are few observable counterparts to the textbook experiment of shifting an industry’s demand curve while leaving its supply curve unchanged. Instead, most observable shocks—such as changes to monetary policy and exchange rates—impact both demand and supply. For example, consider an industry’s response to an unexpected devaluation in the dollar relative to the euro. This makes European producers’ goods more expensive, so it increases demand for U.S. producers’ goods. However, the devaluation also increases the cost of U.S. producers’ inputs imported from Europe. This cost increase reduces the supply forthcoming from U.S. producers at any given price, and so mitigates the demand effect. Goldberg and Campa document that movements in the exchange rate significantly impact manufacturing industries through both these channels.2 The expected industry growth following the dollar’s devaluation may fail to materialize because the expansion of demand has been offset by a contraction in supply. For this reason, exchange rate fluctuations are not directly useful for measuring industries’ responses to demand shocks.

To overcome this difficulty, we use a unique natural experiment to disentangle the demand and supply effects of exchange rate shocks on retailers located on the U.S.–Canada border. Because dollar-denominated prices adjust only slowly to exchange rate changes, a change in the exchange rate causes the same good to sell for different real prices on opposite sides of this border. Subsequently, both countries’ border residents shift their expenditures toward the cheaper country, thereby increasing demand in its border area. The same exchange rate change also affects retailers’ costs and hence industry supply, but this cost effect is likely to be shared by all retailers. This allows us to use an experimental methodology in our measurement, where retailers from interior areas serve as a control group for a treatment group of retailers near the border. Differences between the responses of the treatment and control groups to a change in the exchange rate isolate its demand effects on the treatment group.

We apply this methodology to four industries (by SIC industry)—Food Stores, Gasoline Service Stations, Eating Places, and Drinking Places—using 20 years of county-level observations of the number of employers in each industry and their average employment. Our results indicate that the creation and destruction of new producers play substantial roles in three industries’ immediate and nearly immediate responses to changes in demand.

U.S.–Canada trade and cross-border shopping

Our use of real exchange rate fluctuations to measure responses to demand shocks relies on two assumptions. First, movements in the real exchange rate do not present arbitrage opportunities that would cause U.S. border retailers’ costs to systematically differ from those of their counterparts in the country’s interior. This allows retail industries in the interior to serve as a control group for those on the border. Second, these same movements induce border area consumers to shift their expenditures between U.S. and Canadian border retailers. Consumers’ observed cross-border shopping decisions reinforce both of these assumptions.

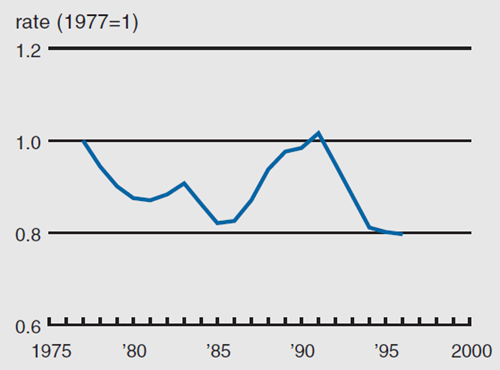

U.S. and Canadian consumers can cross the border for recreational purposes, subject only to a (usually) brief customs inspection. Furthermore, they can import small quantities of goods for personal use. Figures 1 and 2 illustrate how consumers take advantage of price differences to shift their expenditures toward the low-price country. Figure 1 depicts the Canada–U.S. real exchange rate between 1977 and 1996, normalized to equal one in 1977. This is the two currencies’ market exchange rate multiplied by the ratio of their consumer price indices (CPIs). Hence, it measures the purchasing power of the Canadian dollar after being exchanged for U.S. dollars and spent in the U.S. The Canadian dollar’s real value (in the U.S.) dropped substantially between 1977 and 1985. This decline reversed in the late 1980s, but this proved to be temporary. Between 1991 and 1996, the Canadian dollar lost 20% of its real value in the U.S.

1. Real exchange rate

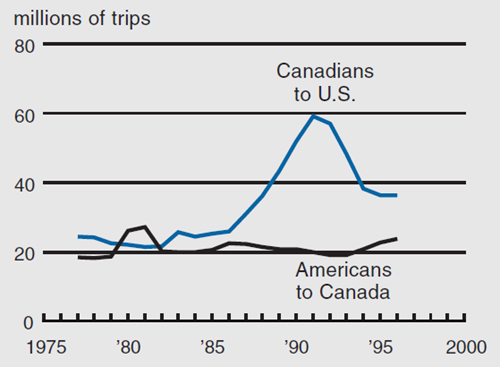

Figure 2 plots the number of trips from one country to the other that last one day or less. This variable is the official measure of cross-border shoppers used by Canadian government agencies. During the appreciation of the Canadian dollar between 1986 and 1992, the number of Canadian one-day trips increased dramatically, reaching a peak of approximately 59 million during 1991. The flow of cross-border shoppers reversed direction when the Canadian dollar subsequently depreciated: American one-day trips to Canada climbed from 19 million in 1992 to nearly 24 million in 1996. The spike in American trips in 1980 and 1981 came at a time when the Canadian National Energy Policy subsidized petroleum imports and taxed exports. These policies greatly reduced the price of gasoline in Canada relative to the U.S., and American consumers took advantage of the opportunity to fill their tanks tax-free. The export tax was much more easily enforced against large tanker trucks, so the same price difference presented no arbitrage opportunity to wholesalers.

2. Same-day trips

The extent and timing of cross-border shopping indicates that wholesale arbitrage does not eliminate international price differences near the border. That is, it is considerably easier for consumers to shift their expenditures on retail goods and services than it is for retailers to shift their expenditures on inputs.

Data and methodology

Our observations of retail trade industries come from the U.S. Census’ annual publication, County Business Patterns (CBP) from 1977 through 1996. In each county and for each of the four industries we consider, the CBP reports the industry’s March employment and the total number of establishments with employment during the year. These two variables are the basic objects of our analysis. We focus on counties in the ten contiguous states that border Canada, so that the interior counties are otherwise as similar as possible to the border counties, and on counties with populations greater than 20,000 people, as measured in the 1990 decennial census. There are 256 such counties in the ten states, and 19 of them share a border with Canada. The data from these counties comprise our sample.

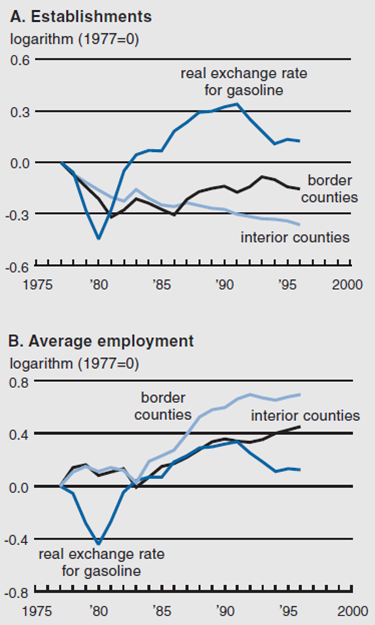

Figure 3 provides an impression of our data for one industry, Gasoline Service. Panel A plots the number of establishments (in logarithms) in the border and interior counties. Panel B plots the logarithms of employment per establishment (average employment) in border and interior counties. Both panels also contain the logarithm of the relative price of gasoline between the U.S. and Canada. This series was calculated as the two countries’ exchange rate multiplied by the ratio of Canada’s CPI for gasoline to that from the U.S.

3. Gasoline Service Stations

Between 1977 and 1981, the price of gas in Canada fell 44% relative to the U.S. During this period of high oil prices, the number of Gas Service establishments declined in both border and interior counties, but the decline was much greater in border counties. There were 30% fewer establishments in border counties in 1981 than in 1977, and the corresponding number for interior counties is 20%. If we use the interior counties as a control group for the border counties, then the treatment of shifting demand for gasoline away from the U.S. resulted in a 10% drop in establishments. In contrast, Gasoline Service’s average employment in border and interior counties was nearly identical. Thus, it appears that retail gasoline industries in border counties shrank and recovered through this period by adjusting the number of establishments. Between 1985 and 1991, when gasoline became relatively cheap in the U.S., the number of establishments in border counties grew by approximately 10%, while the number in interior counties shrank by 3%. Gasoline Service’s average employment grew in both border and interior counties, but it grew by much more (40% versus 20%) in border counties. Overall, figure 3 shows that changes in both average establishment size and in the number of establishments were used in border counties’ retail gasoline industries to accommodate the demand shifts due to cross-border shopping. Movements in the number of establishments were particularly important during the oil-shock period, when Canadian gasoline was very inexpensive.

Econometric results

To quantify the demand-shifting effects of real exchange rates, we have estimated an econometric model in which the number of establishments in a county and their average employment depend on their own values in the previous year and a shock that is common to all counties. For border counties, the current and past year’s real exchange rates also influence both industry variables. The presence of common shocks controls for factors that influence retailers in both border and interior counties, so the estimated effects of real exchange rates reflect only the demand effects from cross-border shopping.

Because there is no reason to expect our four industries to respond similarly to the real exchange rate, we have estimated our model for each of them. As in figure 3, the real exchange rates are industry specific. For example, we construct the real exchange rate using the two countries’ CPIs for Food Away from Home when estimating the model for Eating Places.

The model accommodates persistent differences across counties in two ways. First, we allow the average values (over time) of the number of establishments and their average employment to differ across counties. Second, the influence of the real exchange rate on a county’s retail industry depends on the importance of the local Canadian market. Thus, retail industries in a small U.S. county located next to a larger Canadian city (such as St. Clair County, Michigan, next to Sarnia, Ontario) will respond more to the real exchange rate than will their counterparts in a large U.S. county with a smaller Canadian counterpart (as in Wayne County, Michigan, next to Windsor, Ontario).

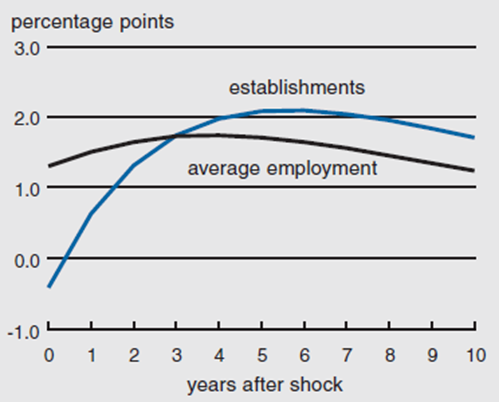

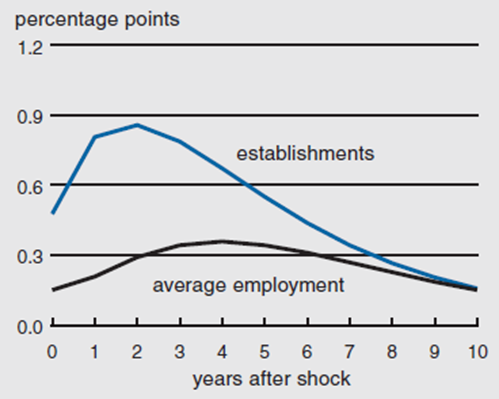

Figures 4 and 5 plot simulations from the estimated models for two of the industries we consider: Gasoline Service and Eating Places. The latter includes food service establishments with and without table service. The blue lines plot the responses of the number of establishments serving a county to a persistent increase in the real exchange rate, and the black lines plot the responses of establishments’ average employment to the same disturbance. The simulated paths for the number of establishments and their average employment are expressed as percentage differences from their initial values. Because we measure the real exchange rate as the value of the Canadian dollar in the U.S., we expect these increases to shift expenditures toward the U.S., expanding retail trade industries in border counties.3 The half-life of the real exchange rate change for Gasoline Service is 5.4 years and it is 2.4 years for Eating Places. We chose the sizes of the real exchange rate changes and their half-lives to match the real exchange rate’s variability and persistence in our data.

4. Simulation for Gasoline Service

5. Simulation for Eating Places

The estimates for Gasoline Service reflect both the strong response of the number of establishments to the period of cheap Canadian gasoline and the adjustment of both variables in the late 1980s as the price of gas increased. Immediately following the real exchange rate increase, the number of employees per establishment rises more than 1%, and the number of establishments serving the industry declines slightly. This decline is not statistically significant. Thereafter, the increase in average employment persists as the number of establishments rises. After five years, the number of establishments has increased by approximately 2%. Thus, Gasoline Service’s transition from the short run to the long run apparently begins after one year. This is considerably less than the half-life of the underlying disturbance, so we conclude that variation in the number of establishments is an important characteristic of this industry’s short-run fluctuations.

Changes in the number of establishments play a central role in Eating Places’ responses to the real exchange rate. In the period of the exchange rate change, the number of establishments increases by 0.5%. The number continues to grow in the first year and hits its peak of 0.86% above its initial value in the second year. As the real exchange rate change dissipates, the number of establishments returns to its initial level. Eating places’ average employment displays almost no response at any horizon to the real exchange rate change. Apparently, long-run industry analysis, in which the industry accommodates changes in demand by changing the number of producers while keeping the output of each producer fixed, characterizes this industry’s short-run fluctuations. That is, the transition from the short run to the long run in this industry is very rapid.

For Food Stores, the number of establishments responds one year after an increase in the real exchange rate. We conclude for this industry that fluctuations in the number of establishments contribute significantly to its short-run fluctuations. Finally, the responses of Drinking Places to a real exchange rate change are quite different from the others. The number of employees per establishment rises dramatically when alcoholic beverages in Canada become more expensive than in the U.S., and the number of establishments hardly changes. This possibly reflects the well-known licensing restrictions on alcohol sales.

Conclusion

Much of microeconomic theory assumes that the entry of new producers responds to persistent shocks only in the long run, so that incumbent producers can temporarily earn economic profits following a favorable aggregate demand or cost shock. Our results shed light on the speed of the transition to the long run in four retail trade industries. In Drinking Places, persistent demand shocks arising from cross-border shopping affect industry activity without changing the number of establishments. We infer from this that the transition to the long run in that industry is very slow. In the other three industries we consider, either potential entrants, incumbent producers considering exit, or both respond relatively rapidly to demand shocks.

Notes

1 Campbell and Lapham, 2002, “Real exchange rate fluctuations and the dynamics of retail trade industries on the U.S.–Canada border,” Federal Reserve Bank of Chicago, working paper, No. 2002-17.

2 Linda S. Goldberg and José Campa, 1997, “The evolving external orientation of manufacturing: A profile of four countries,” Federal Reserve Bank of New York, Economic Policy Review, Vol. 3, No. 2, pp. 53–81.

3 Our model is linear, so the predicted responses to a persistent decrease in the real exchange rate will have the same pattern but with the opposite sign. That is, figures 4 and 5 would be reflected around the horizontal axis if we had instead considered a decrease in the real exchange rate.