Results from a Special Chicago Fed Survey of Business Conditions on Remote Work

At the onset of the Covid-19 pandemic, many workplaces in the U.S. were closed (either voluntarily or by government order) to limit the spread of the virus. Some of these workplaces, such as factories, reopened within a few months. Yet many other workplaces remained closed, and the vast majority of their employees continued to perform their tasks off-site. The pandemic has stretched on long enough that for many employees, remote work has become a new normal. But now, with Covid-19 vaccines widely available in the U.S., many long-closed workplaces are starting to reopen, and workplace leaders are implementing return-to-office plans. To what extent have employees been working remotely since the pandemic began? And to what extent might employers continue remote work arrangements into the future? In this blog post, we present answers to those questions from a special Chicago Fed Survey of Business Conditions (CFSBC), which was conducted during the period of July 12–16, 2021.

We received 135 responses from leaders of business and nonbusiness organizations representing a wide range of industries, as shown in table 1. While the CFSBC is not a representative sample of employers in the Seventh Federal Reserve District, aggregate results from a survey question on economic activity have been shown to track the macroeconomy quite well in the past. For the results that follow, we have split the respondents into two groups: goods producers and service providers. We do this because goods producers generally have much less flexibility than service providers when it comes to letting their workers telecommute.

Table 1. Distribution of respondents’ industries

| Sector | Number of respondents | Share of respondents |

|---|---|---|

| Goods producers | 73 | 54 |

| Construction, real estate, and utilities | 20 | 15 |

| Manufacturing | 45 | 33 |

| Transport, warehousing, and wholesale trade | 8 | 6 |

| Service providers | 62 | 46 |

| Arts, entertainment, recreation, accommodation, and food services | 2 | 1 |

| Administrative, public administration, and other services | 13 | 10 |

| Educational and health care | 6 | 4 |

| Finance | 25 | 19 |

| Professional, scientific, and technical services | 16 | 12 |

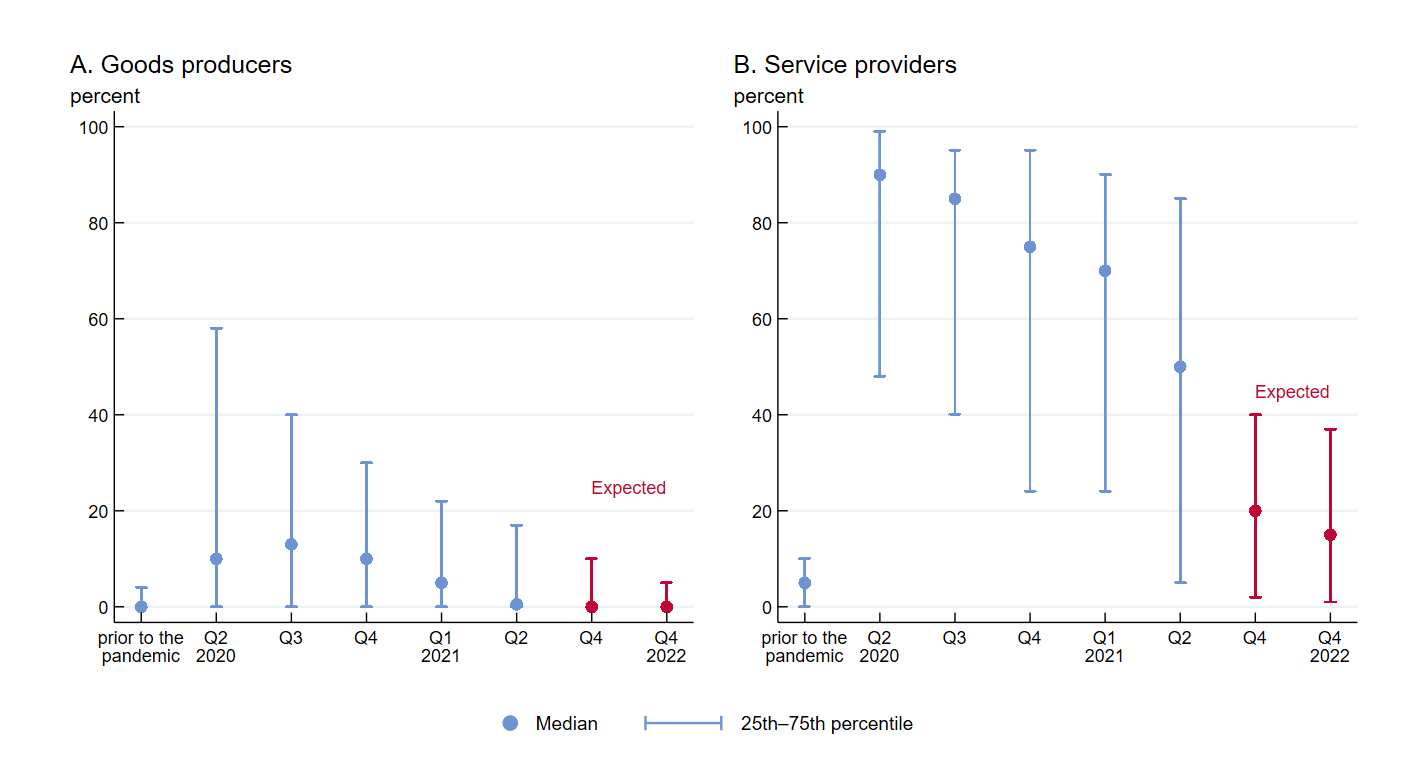

In the survey, we asked respondents to estimate the share of their organization’s workforce that worked remotely four or more days per week prior to the pandemic and then in each quarter since the pandemic started. For the rest of this blog post, working remotely is defined as telecommuting a minimum of four days per week. We also asked about their expected shares of remote workers at the end of 2021 and 2022. Figure 1 displays the distribution of responses. The dots represent the median response and the vertical lines with caps show the 25th to 75th percentile range of responses. Before the pandemic, most organizations in both the goods and service sectors reported similar shares of remote workers—only a small percentage of their workers were working remotely. Among goods producers, the median share of remote workers was 0%, and among service providers, the median share was 5%.

Figure 1. Share of workforce working remotely four or more days per week

Source: Authors’ calculations based on data from the Federal Reserve Bank of Chicago, Chicago Fed Survey of Business Conditions.

When the pandemic hit the U.S. in March 2020, there was a shift in the share of remote workers for most organizations, but the size of the shift varied dramatically depending on which sector the organization was in. According to the survey, in the second quarter of 2020, the median share of remote workers for goods producers increased to 10%, but this share spiked to 90% for service providers. The vertical lines indicate that there was a wide range of responses within both sectors. Since the second quarter of 2020, the share of remote workers has been steadily declining in both the goods and service sectors (for the goods sector, the median share moved up between the second and third quarters of 2020, but the 75th percentile share moved down).

Covid-19 vaccines became widely available in the second quarter of 2021. For that quarter, the median goods sector respondent reported a nearly full return to in-person work, but the median service sector respondent reported around 50% of their workforce was still telecommuting. Also for that quarter, we saw the largest 25th to 75th percentile range in responses among service providers; this reflects the fact that some workplaces in the service sector made significant changes in remote work arrangements during that time, whereas others did not.

Turning to forecasts for the share of remote workers, we find that goods producers expect to be close to their pre-pandemic shares by the fourth quarter of 2021. That said, many goods sector respondents commented that middle- and senior-level management will likely still have the option to continue working remotely at that time. Service sector respondents do not expect to be back to their pre-pandemic shares of remote workers by the fourth quarter of 2021, but they do expect many more workers to be on-site by year’s end than there are now; the median service sector respondent anticipates the share of remote workers to be down to 20%. That share may turn out to be higher because the survey was fielded in mid-July 2021, before the recent nationwide growth in the rate of new daily Covid-19 cases.

Unlike the goods sector respondents, many service sector respondents expect the increase in the share of remote workers to stick around longer term. For the fourth quarter of 2022, the median service sector respondent projects that 15% of their workforce will be remote—much higher than the pre-pandemic share of 5%. Multiple respondents from the service sector commented that their respective organizations had made working remotely for some workers permanent and that they were offering others the option to work remotely on a part-time or full-time basis. Most service sector respondents indicated that they expect workers whose tasks can be done remotely to spend more time telecommuting than they did before the pandemic.

The results of this special CFSBC suggest that the pandemic has fundamentally altered the way many organizations will conduct their post-pandemic operations. Most workers are likely to be at a workplace away from home most of the time. However, more workers are expected to be full-time remote than before the pandemic, and the option to be part-time remote is expected to be more common.