The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

Potential reductions in defense spending raise the issue of how these reductions will affect local and regional economies. One important issue is the dollar amount of the reduction. Regions that received proportionately greater defense funds stand to lose more by spending cuts. Another issue is the kind of product supplied by the region. A firm selling screwdrivers to the Pentagon can probably find other markets for its product; whereas, a firm selling aircraft weapons systems may have more problems. Thus, a region supplying weapons systems to the military will be hurt more by cuts in defense spending than a region supplying screwdrivers.

Measuring the economic impact of spending cuts on a region’s economy is more complicated than it might first appear. Clearly, a reduction in defense spending will affect defense contractors. These are the direct effects of a spending cut. There may also be indirect effects, as the firms supplying goods and services to defense contractors are also affected. One way to measure the economic impact of a change in spending is to use an Input-Output (I-O) model, which provides an estimate of the change in output, taking into consideration both direct and indirect effects, for a given change in defense procurements.

In this Chicago Fed Letter, we analyze the impact of defense spending on the Chicago economy using our Chicago I-O model.1 In particular, we estimate the direct and indirect effects of defense purchases on employment and income of different sectors in the Chicago economy. Based on these estimates, regional analysts can judge the importance of defense funds not just by the dollar amount of direct expenditures but by their overall impact on the regional economy.

Chicago defense procurement funds

In 1987, total Chicago defense procurement funds (CDPF) consisting of military contracts awarded to Chicago producers amounted to $1.06 billion ($.97 billion in 1982 dollars as reported in figure 1). This amount is disproportionately small relative to both total national defense procurement funds and total Chicago economic activity.

1. Chicago versus United States, 1987

| Chicago | U.S. | Chicago's share % | |

|---|---|---|---|

| (Billions of 1982 dollars) | |||

| Gross product | 129.33 | 3,846.2 | 3.36 |

| Total output | 235.03 | 7,051.7 | 3.33 |

| Total income | 73.68 | 2,352.6 | 3.13 |

| Federal tax receipts | 21.71 | 711.1 | 3.05 |

| Defense procurements | 0.97 | 120.1 | 0.81 |

| (Millions) | |||

| Total employment | 4.00 | 132.9 | 3.01 |

| Total population | 6.66 | 244.0 | 2.73 |

Total national defense procurement funds for 1987 were $133.4 billion ($120.1 billion in 1982 dollars as reported in figure 1), hence the CDPF share represented only about 0.8% of the national total. The CDPF represented .75% of Chicago’s total output of goods and services and 1.3% of Chicago’s total personal income in 1987. Also, Chicago’s share of national defense procurement funds was much smaller than its share of national economic activities. For example, Chicago’s population, employment, gross product, and tax revenues each comprised between 2.7% and 3.4% of the corresponding national totals, as shown in figure 1.

In general, the discrepancy between a region’s share of total national economic activities and its share of total procurement funds can be explained by the fact that regions with the available capacities for producing defense-related goods often receive a relatively larger share of defense procurement contracts. Because funds are awarded for the production of goods and services rather than for investments in new production facilities, a region’s share of procurement funds will be relatively low if it does not have the appropriate infrastructure. Consequently, Chicago receives a disproportionately low share of procurement funds because it does not have the necessary facilities for producing many goods required by the defense department.

Figure 2 presents the share of CDPF relative to national procurement funds. These data show that the major fund recipients in Chicago do not necessarily correspond to the major fund recipients at the national level. For example, business services, which includes research and development, obtains the second largest share of procurement awards for both the nation and Chicago. However, transportation equipment, which includes airplanes and naval ships, obtains the largest share of the national defense procurement awards, accounting for 40% of awards, while in Chicago this sector accounts for less than 3% of awards. Chicago does not have the physical facilities to produce military airplanes and large ships. On the other hand, Chicago’s close proximity to the nation’s agricultural heartland and its extensive transportation network give it an advantage in food processing. Thus, while purchases of processed food accounted for less than 0.6% of the national defense procurement awards in 1987, this sector accounts for almost 5% of Chicago’s defense procurement awards, a concentration more than eight times the national level. This example illustrates the fact that the distribution of procurement funds across sectors is not equal in every region. Rather, the Chicago region, for example, specializes in its own set of products demanded by the military.

2. 1987 defense expenditures by sector

| Chicago funds | U.S. funds | ||||

|---|---|---|---|---|---|

| Percent of total | Rank | Percent of total | Rank | ||

| Electrical machinery | 42.08 | 1 | 8.29 | 3 | |

| Personal & business services | 21.85 | 2 | 19.85 | 2 | |

| Construction | 6.91 | 3 | 6.25 | 4 | |

| Food & kindred products | 4.77 | 4 | 0.58 | 14 | |

| Scientific & control instruments | 4.76 | 5 | 6.05 | 5 | |

| Chemicals & allied products | 3.04 | 6 | 3.51 | 7 | |

| Machinery, except electrical | 2.93 | 7 | 3.06 | 8 | |

| Transportation equipment | 2.49 | 8 | 40.00 | 1 | |

| Fabricated metals | 2.23 | 9 | 3.86 | 6 | |

| Health, education, & nonprofit | 1.82 | 10 | 0.72 | 13 | |

| Total | 92.88 | 92.17 | |||

Input-Output analysis of the CDPF

Defense purchases increase the demand for goods and services, which boosts Chicago economic activity. However, the amount of CDPF alone cannot measure the extent of Chicago economic expansion resulting from such external demand. One reason is that the external demand represented by CDPF funds could be satisfied by importing goods and services from other regions rather than by production in Chicago. If the entire CDPF demand was satisfied by imports from other regions into Chicago, the benefit to Chicago production would be 0. On the other hand, if local producers satisfied the entire CDPF demand without imports from other regions, then Chicago would receive the full benefit of the expenditures. These polar cases show that the CDPF amount alone cannot be used to measure the effect on the regional economy. The I-O model determines the employment and income generated by defense procurement funds and thus determines the extent to which military demand for goods and services is satisfied by Chicago producers rather than imported goods.

Another reason the CDPF amount is not an accurate measure of the effect of military demand for goods and services on the local economy is that each dollar spent on goods in one sector may increase the demand for goods in other sectors. That is, the demand for military goods and services has both direct and indirect effects. An important part of the use of I-O models is to analyze the indirect as well as the direct effects of changes in demand for goods and services.

Consider the food processing industry, which produced $48.1 million of goods for procurement contracts. To produce that bundle of goods, this industry purchased $1.5 million of business services, $1.2 million of transportation and warehousing services, and so on. These are the indirect effects of the demand for food by the military. In addition, each of the suppliers to the food processing industry purchased other materials and services, which are included in the indirect effects of the demand for food by the military. The I-O model captures the entire chain of direct and indirect purchases.

The military demand for goods and services also creates what is called an induced effect. Both the direct and indirect suppliers of goods for the military employ workers who demand goods and services. This demand is the induced effect of the military procurements. The indirect and induced effects can be a substantial part of the total demand effect. For example, the production of food purchased by the military does not require significant direct purchases of services from the finance and insurance sector, yet the indirect and induced demand for this sector’s services was $1.2 million, equal to the food processing industry’s demand for transportation and warehousing. Although the food processing industry’s demand for transportation and warehousing was substantial, at $1.2 million, when indirect and induced demand are included, the total demand for these services rises to $2.8 million. Overall, while this $48 million in defense contracts created only $15.2 million in direct purchases by the food processing industry, the total effects, including indirect and induced effects, amounted to $88.6 million.

In diversified regions such as Chicago, indirect effects produce the greatest benefit for service industries such as business services, health, utilities, transportation, and retail trade. This is because each industry involved in exporting goods and services out of the region will purchase many of these services within the region. Moreover, individuals will make further contributions to the growth of these sectors through the induced effect of their earned income. For example, the food sector sells its output to consumers that received wages from companies that received CDPF expenditures. For a given sector, the indirect and induced effect from other sectors’ growth can exceed the direct CDPF impact. One benefit of I-O analysis is that it identifies sectors receiving substantial indirect or induced effects. This can be useful information. For example, firms in sectors with large impacts but few direct military contracts may want to consider joining the lobbying efforts for procurement funds. Another, perhaps more important, benefit is that this analysis allows a ranking of the overall effect of each industry’s export on the regional economy, which provides regional leaders with priorities on the choice of a procurement program.

Empirical results

The data in this study are for the Chicago Metro Area which consists of 6 counties: Cook, DuPage, Kane, Lake, McHenry, and Will. All data are for 1987. The choice of 1987 was dictated by the availability of the Chicago I-O model. Two major data sets were necessary for the analysis: the Chicago I-O table and the data on the defense procurement purchases. Data were aggregated into 36 sectors.

Figure 3 lists employment and income added to the Chicago economy due to the direct, indirect, and induced effects of the CDPF, as derived from the Chicago I-O model. CDPF purchases of $1.06 billion generated 36,728 jobs and $761.3 million of additional income, amounting to 0.9% of Chicago employment and 0.9% of Chicago income. These percentages are slightly larger than the share of CDPF in Chicago gross product, which was 0.75%. This result indicates that, because of indirect and induced demand effects, one dollar of defense purchases generates more employment and income on average than one dollar of Chicago gross product. This is because the CDPF is concentrated in those industries with high multipliers (as shown in figure 3). Multipliers represent the total effect on the economy of each dollar of demand for an industry’s goods. It follows that the inputs for CDPF goods are manufactured locally, rather than imported, to a greater extent than the inputs for production of Chicago’s gross output.

3. Total effect of Chicago defense funds, 1987

| Employment | Income | ||||||

|---|---|---|---|---|---|---|---|

| Thousands | Rank | Multiplier (jobs/$million) | $millions | Rank | Multiplier (cents/$) | ||

| Electrical machinery | 5.837 | 2 | 28.3 | 140.712 | 2 | 60.2 | |

| Personal & business services | 12.346 | 1 | 57.9 | 249.794 | 1 | 114.9 | |

| Construction | 1.015 | 7 | 34.5 | 28.690 | 6 | 78.3 | |

| Food & kindred products | 0.773 | 10 | 17.4 | 21.218 | 8 | 37.8 | |

| Scientific & control instruments | 0.428 | 14 | 20.6 | 11.469 | 13 | 45.2 | |

| Chemicals & allied products | 0.456 | 12 | 20.5 | 14.634 | 11 | 47.7 | |

| Machinery, except electrical | 0.327 | 18 | 18.0 | 8.771 | 15 | 39.6 | |

| Transportation equipment | 0.239 | 21 | 22.7 | 7.246 | 19 | 52.8 | |

| Fabricated metals | 0.564 | 11 | 22.2 | 14.857 | 10 | 50.1 | |

| Health, education, & nonprofit | 2.742 | 4 | 50.1 | 53.349 | 3 | 97.0 | |

| Total of all industries | 36.728 | 761.274 | |||||

In summary, figures 1-3 show that employment and income generated by the CDPF in different sectors of the Chicago economy are not highly correlated with the initial CDPF expenditures in that sector. For example, the food processing sector is ranked fourth in funds received (figure 2) yet ranks only tenth in employment effects and eighth in income effects (figure 3). This variance in rankings is due to the low multipliers. Another example is transportation equipment, which ranks eighth in total funds received but only 21st and 19th in employment and income effects. This indicates that the Chicago economy rearranges the distribution of initial CDPF spending to fit the production capabilities and sales patterns of Chicago producers and consumers. This redistribution is represented in the I-O model as the indirect and induced effects of initial CDPF spending.

Conclusions

Chicago, like the Seventh District as a whole, received a small portion of defense procurement funds, due in large part to a mismatch between military needs and the region’s industrial specialization. While this may be bad news for the region in times of military escalation, in today’s environment of expected reductions in defense spending it means that the Chicago economy will not be drastically affected. Moreover, Chicago’s specialization in defense procurement contracts is structured toward products that suit the civilian market, namely electrical machinery, business services, food, and control instruments (which represent 73% of the total funds). These sectors are well equipped to make the transition from the defense to the civilian and export markets.

The defense fund reductions, however, may affect the direct recipient’s sector to a lesser degree than other sectors of the economy. For example, a decline of funds to the food sector will affect the business services sector by a greater degree than the food sector itself. Finally, the evaluation of the defense procurement impacts on the Chicago economy should be based on the total multiplier effect, because the dollar value of the defense program may not reflect the total impact on the region. The strong variations across Chicago’s multipliers indicate that equal cuts in funds going to different sectors of the economy will have significantly different effects on the economic welfare of the region.

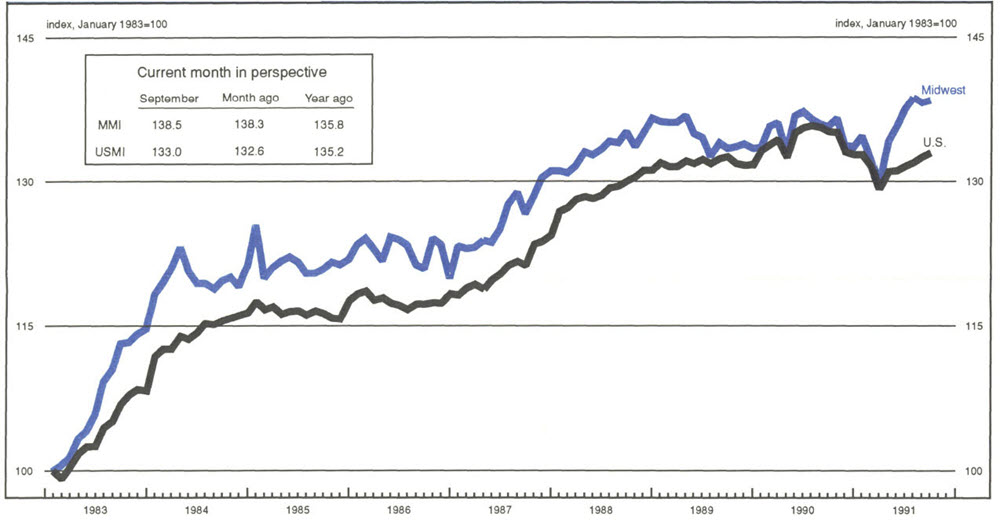

MMI-Midwest Manufacturing Index: Current expansion

Manufacturing activity in the Midwest edged up 0.2% in September, despite weakening in many of its industries. Gains were posted by metal fabricating, machinery, and an assortment of nondurable goods producing industries. However, weakness emerged in primary metals and transportation equipment industries. Cutbacks in auto production schedules in the fourth quarter are likely to contribute to declines in auto-related industries over the remaining months of 1991.

Midwest manufacturing gains in September were slightly below nationwide growth, up 0.3%, and the Midwest has advanced at about half the national rate over the three-month period ending in September. However, the Midwest is still outperforming the nation since the end of the recession.