The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

After growing by 4.5% during 1997 and by 4.3% during 1998, the economy slowed down a bit in the first half of 1999, expanding in the first quarter by 3.7% and in the second quarter by just under 2%. However, the economy found its wings in the third quarter and grew by a robust 4.8%. The consumer was the key driving force during 1999.

Consumer spending rose by 3.7% during 1997 and then accelerated to a very strong 4.9% rate in 1998. During the first quarter of 1999, consumer spending increased by 6.5%, followed by a 5.1% increase in the second quarter and a 4.3% rise in the third. As the year drew to a close, it was obvious that light vehicle sales would set a record, exceeding that set in 1986 by over half a million vehicles. Housing starts were the strongest of any year in the current expansion, even with increasing mortgage rates during the year. The unemployment rate reached its lowest level in over 30 years. Inflation, which had averaged 1.6% during 1998, began to increase during the middle of 1999 as world economies improved. Inflation averaged 1.5% for the first quarter of 1999, rose to 3.5% in the second quarter, and then moderated a bit to 2.6%. Continuing economic strength and concerns about inflationary pressures led the Federal Reserve to increase the fed funds rate by 25 basis points three times beginning at the end of the second quarter of 1999. It was in this setting that the Federal Reserve Bank of Chicago held its 13th annual Economic Outlook Symposium on December 4, 1999. More than 60 economists and analysts from business, academia, and government attended the conference. This Chicago Fed Letter reviews the accuracy of last year’s conference forecast for 1999 and summarizes the presentations at this year’s conference.

Looking over our shoulder

The benchmark revision to the National Income and Product Account data in October 1999 make the comparisons between the actual performance of the economy in 1999 and the forecasts from last year’s symposium less meaningful. In essence the benchmark revision raised historical gross domestic product (GDP) growth by around 0.5 percentage points. Not surprisingly, this led to the strength of the economy during 1999 being significantly underestimated. Last year’s symposium participants expected real GDP to increase by just over 2% during the first three quarters of 1999; based on the revised benchmark, growth averaged 4% over the period. This underestimation was true for most of the subcategories of GDP. The 2.2% growth rate of industrial production for the first three quarters was just a bit higher than the 1.6% rate forecast. Light vehicle sales averaged 1.84 million more units than forecast. Housing starts were expected to moderate to a 1.50 million-unit rate after a very strong year in 1998. Instead, housing starts for the first three quarters of 1999 were even higher than in 1998, adding 1.68 million units. The trade-weighted dollar was anticipated to increase a slight 0.6% during the first three quarters of 1999; however, the dollar was 2.7% lower during this period. An overestimation of 0.5 percentage points occurred for the unemployment rate forecast. The forecast for inflation was right on target at 2% for the first three quarters of 1999, following the 1.6% average of 1998. The interest rate forecasts were too low by approximately 50 basis points for the first three quarters of 1999. In summary, the economy expanded faster, inflation was as anticipated, and unemployment rates were lower than symposium participants anticipated.

Looking ahead

For 2000, the forecasters expect the positive 1999 economic conditions to continue, albeit at a slower pace. The general conclusion was that Y2K is not a significant economic concern. Figure 1 summarizes the forecasts for 1999 (fourth quarter numbers not known) and 2000. The typical forecaster is expecting real GDP growth of 3.8% in 1999 and 3.1% in 2000. Most forecasters at the symposium took the view that the 1999 growth rates are unsustainable and that real output growth during 2000 will be lower for every subcategory of GDP. Personal consumption expenditures, business fixed investment, residential construction, and government spending growth are forecast to slow in 2000. Change in business inventories is expected to increase slightly from $34.3 billion in 1999 to $37.5 billion in 2000. Net exports are forecast to decline from –$324.6 billion in 1999 to –$349.6 billion in 2000.

1. Actual 1998 and median forecasts of GDP and related items

| 1998 | 1999 | 2000 | |

| (Actual) | (Forecast) | (Forecast) | |

| Real gross domestic producta | 4.3 | 3.8 | 3.1 |

| Real personal consumption expendituresa | 4.9 | 5.1 | 3.3 |

| Real business fixed investmenta | 12.7 | 9.1 | 6.8 |

| Real residential constructiona | 9.2 | 6.9 | -1.7 |

| Change in private inventoriesb | 74.3 | 34.3 | 37.5 |

| Net exports of goods and servicesb | -215.1 | -324.6 | -349.6 |

| Real government consumption expenditures and gross investmentsa | 1.7 | 3.1 | 2.1 |

| Industrial productiona | 3.7 | 2.4 | 2.7 |

| Auto and light truck sales (millions of units) | 15.5 | 16.8 | 15.9 |

| Housing starts (millions of units) |

1.62 | 1.65 | 1.54 |

| Unemployment ratec |

4.5 | 4.2 | 4.3 |

| Inflation rate (Consumer Price Index)a |

1.6 | 2.2 | 2.6 |

| 1-year Treasury rate (constant maturity)c |

5.05 | 5.10 | 5.47 |

| 10-year Treasury rate (constant maturity)c |

5.26 | 5.62 | 6.10 |

| J.P. Morgan trade-weighted dollar indexa | 5.0 | -2.0 | -3.0 |

b Billions of chained (1996) dollars.

c Percent.

Note: Data as of December 3, 1999.

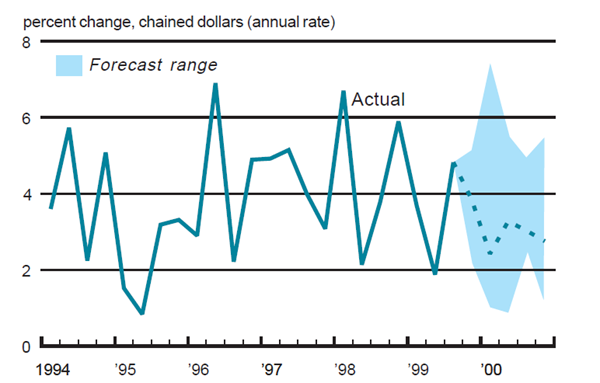

In terms of the quarterly pattern for real GDP, the forecast group is expecting a softer first quarter in 2000 followed by a stronger second quarter, with growth moderating in the third and fourth quarters. In the first quarter, real GDP growth is forecast at 2.4%; it is expected to rise to 3.3% in the second quarter, and then to moderate steadily to 2.8% by the fourth quarter of 2000 (see figure 2).

2. Real GDP growth

Source: U.S. Department of Commerce, Bureau of Economic Analysis.

With the relatively slower growth in real GDP, industrial production growth is anticipated to increase slightly from 2.4% to 2.7% in 2000. After having set a record year in 1999, with 16.8 million units of sales, the light vehicle market is expected to sell 900,000 fewer vehicles in 2000. Housing starts are forecast to moderate to a still robust 1.54 million-units pace in 2000 after having had the best year of the expansion in 1999. With the continued expansion of the economy, the unemployment rate during 2000 is expected to be just one-tenth of a percentage point above the 1999 level. The 2000 rate of inflation is forecast to rise to 2.6%, 0.4 percentage points higher than in 1999. Short-term interest rates are forecast to rise by 37 basis points during 2000, while longer-term rates are expected to rise by 48 basis points, resulting in a steepening of the yield curve. Finally, the trade-weighted dollar is anticipated to fall by 3%.

Household sector

The chief economist from a large bank reviewed developments in the household sector. In 1999, consumer spending added a significant premium to economic growth, as conditions resulting from the global financial crisis led to an increase in purchasing power. In 2000, the extra purchasing power created by the crisis will be gone, so that spending should moderate. Nonetheless, the household sector should flourish based on strong labor markets.

An important development of the global financial crisis of 1998 was that it “twisted the U.S. economy from a reliance on exports to a reliance on consumers.” Decreasing investor confidence in foreign markets triggered recessions abroad, and a flight to safe investments (particularly U.S. Treasury bonds) pushed down interest rates in the U.S. Low interest rates led to strong home sales and high mortgage refinancing activity, which created an estimated $60 billion in extra cash for consumers. Consumer spending was generally strong enough in 1999 to add a 2.25% premium to economic growth. Toward the end of the year, the flight to safety ended and interest rates began to rise ahead of inflation fears, leading to a significant decline in refinancing activity. Also, the dynamics of falling import prices had disappeared, though prices had not yet begun to rise as excess capacity abroad provided some cushion. Weak foreign demand for oil had depressed oil prices early in 1999, but late in the year, prices rebounded more sharply than expected. All told, consumers lost the gains to purchasing power they had enjoyed at the beginning of the year.

Another important element in the household sector outlook is the changing dynamics of the U.S. economy, from conditions of robust growth and decelerating price inflation to conditions of rising inflationary pressures and tight labor markets, which should lead to accelerating real wages. Large firms base their nominal wage gains for the coming year on two things: the current unemployment rate and last year’s inflation rate from the Consumer Price Index. While inflation has been low, the low unemployment rate is driving up nominal wages and real wages are beginning to accelerate. The economist forecasts that real wages will continue to accelerate through 2000, as unemployment continues to fall, reaching 4% gains in the fourth quarter of 2000. Her conclusion is that household spending growth will moderate in 2000, from 5% for much of 1997–99 to below 3% in 2000. She did caution, however, that her estimate could be on the high side.

Automotive sector

An economist from a Big Three auto manufacturer reviewed the automotive sector’s performance in 1999 and presented the outlook for both the near and long term. In 1999, a strong household sector coupled with high incentive activity by auto makers contributed to a record year of light vehicle sales. In 2000, the economist expects some of those fundamentals to change and sales to decline. The economist did see signs of improvement for the long-run trend of vehicle sales.

Most of the variables that indicate consumers’ ability to buy vehicles were sound in 1999. Inflation was low and relatively stable. Growth of real disposable income per household had been relatively flat for two years and showed no sign of decreasing. One of the strongest leading indicators of a recession, the Treasury yield curve (ten-year T-note rate minus the one-year T-bill rate), showed no signs of inverting. The economist did express some concern about consumer debt payments, because repayments were above their previous peak, though there did not seem to be any signs of a sharp acceleration.

Indicators of consumers’ willingness to buy vehicles were also very positive in 1999. Consumer attitudes were near all-time highs, despite a small decline in the summer. Initial unemployment claims were at very low levels. The average manufacturing workweek showed that factories worked overtime for much of the year, indicating increased income. The stock market, an ex-post signal of consumer attitudes, caused some concerns during the fall, but when the Dow rebounded to above 11,000, the market ceased to be a drag on consumer willingness to buy.

The economist divided the strong 1999 vehicle sales into the components that contributed to the high levels: the trend sales level, the wealth effect, incentives, and the general economy. The trend sales level was about 15.4 million units in 1999. The wealth effect added between 0.6 million and 0.8 million units to the trend. The high level of incentives offered by manufacturers added between 0.5 million and 0.8 million units. The strength of the economy, mortgage refinancing activity, and other factors contributed 0.3 million to 0.8 million units, bringing the total for the year to about 17.3 million units. For 2000, the trend should advance to 15.5 million units, the wealth effect should contribute 0.4 million to 0.6 million units, and incentives should contribute zero to a more likely 0.6 million units. With the general health of the economy contributing minimally to sales, total vehicle sales for 2000 should be between 15.9 million and 16.7 million units, with an actual company forecast of 16.4 million units.

The long-term trends in the industry indicate not only changes to the trend sales level, but also to the product mix. The U.S. population is getting older and more affluent. That, coupled with a declining taste for smaller cars, suggests that large, expensive vehicles will become a larger share of the product mix. The three determinants of the long-run trend of vehicle sales, change in the number of households, change in the number of vehicles per household, and replacement of scrapped vehicles, all indicate a higher trend. The economist revised his trend growth rate of vehicle sales, from 0.5% per year through 2005 to 0.67%.

Agriculture sector

An economist from a national agricultural organization presented the outlook for the agriculture sector. In 1999, many grain farmers struggled as prices for their outputs remained at low levels—but were saved by a record government payments package—while livestock farmers fared much better. In 2000, the economist looks for grain prices to continue to decline, but less so than in 1999, and for livestock farmers to continue to fare better than grain farmers.

For grains, there is a very close relationship between the level of stocks and prices. Production of corn has exceeded domestic use and exports for the past four years, the longest stretch of excess production ever. This has resulted in five years of increasing stock levels and corresponding price declines. The situation is similar for soybeans and wheat; stocks of wheat increased, even though total use was expected to roughly equal production in 1999. With the decline in prices and slight declines in production, cash receipts for grain farmers declined for the second year in a row.

Livestock farmers fared slightly better in 1999. Average cow/calf returns were positive, commercial beef production was up, and productivity continued to increase. Commercial pork production was up slightly, but monthly average returns per sow were negative for the entire year. Total meat production and consumption were up for the year, and poultry continued to gain share from red meat.

The economist was “cautiously optimistic” for the year 2000. The livestock sector should be in good shape, and the hog market should rebound in the spring. Eventually, some bad weather should lower crop production, which would help prices.

Y2K

The research director from a large consulting firm discussed the potential impact of Y2K on the economy. The consultant felt that there were likely to be disruptions to a degree and small to medium businesses that did not prepare adequately would be likely to go out of business. He noted that the extent of Y2K effects would not be fully known on January 1. Many procedures are monthly or quarterly so some problems might not be discovered until later in the year. As a result, businesses are likely to continue to allocate resources throughout the year to fix problems as they arise. There could be an impact on productivity at the firm level through the first six months of the year. In the wake of declining Y2K spending, spending on E-business should boom, from 20% of all information technology spending in 1999 to more than 50% in 2001. Indirectly, Y2K is likely to have a regulatory effect in the long term. Given a large backlash against Y2K from the public and policymakers, pressures are building for state software development licensing procedures and software accounting rules.

Steel industry

A consulting economist for the steel industry provided the outlook in that industry. Like other sectors, steel was affected by the economic recovery in the rest of the world. The economist said that steel and other commodity prices should rise and that a continually robust U.S. economy and recovery abroad should provide strength for the steel industry in 2000.

A big factor in the health of commodity industries was the recovery in the rest of the world. This has led to increasing commodity prices in the U.S., which should continue in 2000. Commodity prices should return to the levels they were at in late 1997.

Steel shipments should be up 5.3% in 2000 and domestic consumption should be up 0.8% for the year. Recovery in other commodity industries should lead to increased investment in those industries and increased spending for producer durable goods. Demand for steel to produce consumer durables should stay fairly strong. The economist noted that some of the industry’s recovery in late 1999 might have been related to Y2K inventory building and that demand could decline in the first quarter of 2000.

Equipment

A consultant for the equipment industry discussed the construction and agriculture equipment segments. For construction equipment, strong housing starts this year should allow for strong consumption to continue into next year. But, due to changes in the distribution channels for construction equipment, production will probably decline in 2000. The agriculture equipment sector has not fared as well as the construction equipment sector.

For several years, strong housing starts have translated into strong demand for equipment. In 1997 and 1998, the industry had double-digit gains in new equipment sales and though sales only increased 0.8% in 1999, they remained at high levels. Assuming a moderate decline in housing starts combined with no change in commercial construction activity, no change in surface mining activity, slow increases in interest rates, and increased spending on highway construction spending, new equipment sales should decline 8.1% but still remain at high levels in 2000.

As well as economic factors, changes to the distribution channels of construction equipment continue to affect sales. Renting construction equipment has become increasingly popular; rental companies took in nearly as much revenue in 1999 as manufacturers. Manufacturers were encouraging dealers to rent units, but some dealers were reluctant as they perceive holding inventories for rental as a liability.

Farm consolidation and productivity gains in the agriculture sector have contributed to declining sales of farm equipment. Manufacturers have been looking to cut costs by decreasing inventories and improving supply chain management. The average horsepower of equipment sold has increased, but in recent years an increasing popularity in sundown farming and the growing number of golf courses have contributed to growing sales of machines with less than 40 HP.

Conclusion

After taking a breather in the first half of 1999, the economy expanded by a very strong 4.8% in the third quarter. Forecast participants expect the fourth quarter to slow down just a bit to a still strong 3.9%. Growth is expected to moderate further into 2000, in part due to rising interest rates. None of the forecasters are expecting a recession in 2000. This is a very positive sign for an economic expansion that will set a record in February 2000 as the longest in U.S. history.

Note

The authors would like to thank Keith Motycka for valuable assistance in organizing the Economic Outlook Symposium.