The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

With the U.S. economy apparently struggling to continue the longest economic expansion of our nation’s history, the Federal Reserve Bank of Chicago invited economists from business, academia, and government to attend an Economist Roundtable discussion on February 9, 2001, focusing on the outlook for the Midwest economy in 2001 and beyond. This Chicago Fed Letter summarizes the workshop presentations on the economic outlook for the region and the states in 2001.

Midwest economy more cyclical

Early last year, the national economy grew at a white-hot pace, setting a record for the longest economic expansion in our nation’s history. Real gross domestic product (GDP) growth in the first quarter of 2000 was 4.8%, faster than most economists consider a sustainable pace of expansion. Light vehicle sales were 18.2 million units at a seasonally adjusted annual rate (saar), setting a quarterly record, and housing starts were over 1.7 million units (saar). The strong economic pace continued into the second quarter with real GDP growth rising to 5.6%. However, the economy’s growth weakened substantially as the year came to a close. Real GDP growth was 2.2% and 1.1%, respectively, in the third and fourth quarters. In large part, the economic slowdown was due to a weakening manufacturing sector, which struggled with slowing production to match weakening demand. Inventories began to build, and production cuts accelerated as the year came to a close. While most sectors of the economy continue either to have slower growth or to have experienced only modest declines, the manufacturing sector’s declines are the type usually associated with a recession. However, it is not clear that the weakness in the manufacturing sector will spread to the economy as a whole.

While manufacturing has become a smaller part of the Midwest economy, it is still the key distinguishing sector when comparing the Midwest economy with other regions.1 Manufacturing jobs in the U.S. last year were just 0.2% higher than they were at the beginning of this expansion, but Midwest manufacturing jobs increased by 7.9% over the same period. This had the effect of allowing the Midwest’s share of the nation’s manufacturing jobs to rise from 17.6% in 1991 to 18.9% last year. Since overall job growth in the Midwest has been increasing at a faster rate, manufacturing jobs in the Midwest represent a smaller share of total employment in the region. Manufacturing jobs in the Midwest represented 21.3% of all jobs in the region in 1991, but only 19.4% of all jobs in 2000. While manufacturing job growth has been relatively modest over the current expansion, output has grown by quite a bit. Manufacturing output was 58.9% higher in the nation last year compared with 1991, while the Midwest’s output gain was a more striking 82.6%.

Part of the reason for the better performance of the manufacturing sector in the Midwest is that the region tends to have more cyclical industries than the nation. With less than one in five manufacturing jobs, the region produces just under half of all passenger cars, 30% of all light trucks, and nearly 40% of all the steel in the country. These sectors tend to be very procyclical and the Midwest has been enjoying the fruits of a ten-year-old expansion.

When the manufacturing sector experiences a decline, the Midwest economy tends to fall at a greater rate, typically twice that of the national economy. The manufacturing sector appears to have peaked in September of last year and has been declining since then. True to the region’s cyclical performance, more of the weakness has been reflected in the Midwest than in the nation as a whole. Between September 2000 and January 2001, manufacturing employment fell by 0.8% in the nation, compared to a 1.3% decline in the Midwest. Manufacturing output has also taken more of a hit here in the Midwest. Between September 2000 and January 2001, manufacturing output declined by 2% in the U.S., while Midwest manufacturing output contracted by 3.7%, with much greater reductions taking place in the regional auto and steel sectors.

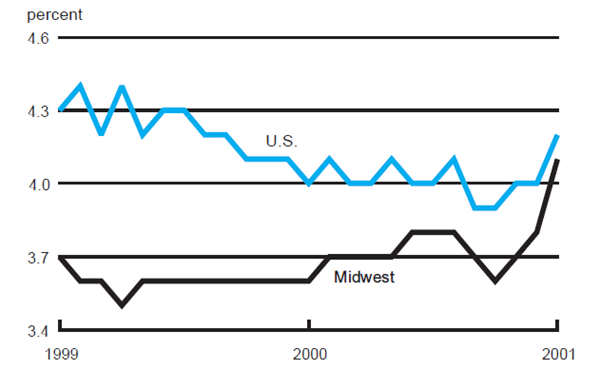

The slowdown in other sectors has also been more pronounced in the Midwest than in the nation. Construction activity has been one area of the national economy that has provided strength in recent months, but while permits for new privately owned buildings in the U.S. were up 9.6% from a year earlier in January, they were up only 2.3% in the Midwest. Nonmanufacturing employment growth in the region has been weaker than in the rest of the country. Sharper increases in jobless claims and unemployment rates (see figure 1) in the Midwest have contributed to more dramatic declines in consumer confidence in the region, and indications are that retail sales in the Midwest have also been weaker than in the rest of the country.

1. Unemployment rates

Source: Bureau of Labor Statistics.

Midwest economy in the year ahead

It is the slowing manufacturing sector that will dictate the path of economic growth for the Midwest in the coming year. While it appears that producers have been quite aggressive at reducing production to control inventories, at the time of the writing of this article an apparent bottom has yet to be reached. Furthermore, the weakness in the Midwest manufacturing sector does appear to have spilled over into other sectors of the regional economy, contributing to weaker performance in the housing market, retail sales, and employment growth. Weak job growth and weak retail sales threaten to put state tax revenues below what many state governments had expected.

The Economist Roundtable group forecast that employment in the Midwest will not show any growth this year and will remain at the levels of last year. While each state is expected to experience slower growth than last year, the two states that are more closely linked with the cyclical vehicle manufacturing industry are anticipated to experience job losses in 2001 compared with 2000. Both Michigan, with 6.4% of its jobs in transportation manufacturing, and Indiana, with 4.3% in that sector, are forecast to lose 0.3% and 1% of their total jobs this year, respectively (see figure 2). Employment in Illinois and Iowa is expected to grow by a modest 0.5% and 0.6%, respectively. Wisconsin is forecast to experience the largest employment growth for the region, rising by 1% in 2001.

2. Employment growth in Seventh District states

| Employment growth rate | Unemployment rate | ||||||

|---|---|---|---|---|---|---|---|

| 1999 | 2000 | 2001 | 1999 | 2000 | 2001 | ||

| year-over-year % change |

end of year, percent | ||||||

| Illinois | 1.0 | 1.2 | 0.5 | 4.2 | 4.5 | 5.1 | |

| Indiana | 1.8 | 1.4 | -1.0 | 3.4 | 2.8 | n.a. | |

| Iowa | 1.8 | 0.7 | 0.6 | 2.5 | 2.5 | 3.0 | |

| Michigan | 1.6 | 2.2 | -0.3 | 3.6 | 3.8 | 4.6 | |

| Wisconsin | 2.4 | 1.9 | 0.1 | 3.2 | 3.3 | n.a. | |

| Seventh District |

1.6 | 1.6 | 0.0 | 3.6 | 3.7 | n.a. | |

Sources: Actual data from the Bureau of Labor Statistics; forecasts (in bold) from Midwest Economist Roundtable participants.

Illinois

Illinois ended 2000 with a rising unemployment rate and declining employment growth, leading the three representatives from Illinois to declare that the state economy is in a slowdown. While one participant acknowledged feeling “skittish” about the economy and another predicted that 2001 will be a “tight” year, none of the participants would say that Illinois is entering a recession.

One sign of weakness is the surge in layoffs late in 2000 and the beginning of 2001. Mass layoffs were up 50%, according to one government labor economist, which contributed to an equal, if not larger, increase in initial unemployment claims. Initial unemployment claims by manufacturing workers were up 30%, while claims by services workers (which includes temporary workers who might work for manufacturers) jumped 80%. The economist analyzed those claimants’ reemployment during 2000. Of the claimants who had worked in the manufacturing sector, 80%–85% had found a job within six months. Of those who had found a job, 75% were back working in the manufacturing sector at about 90% of their former wages. Remarkably, 30% of those who had found employment again were older than 45, an age group that usually finds reemployment difficult. Of the claimants who had worked in the services sector, 75%–80% were back to work in half a year, and 50% of those people were working in the services sector with a 25% pay cut. In a sign of high demand for construction workers, 15% of those claimants from the services sector found new jobs in the construction sector.

Unemployment claims will probably continue to rise through 2001 as employment growth slows. The labor economist sees employment increasing 0.5% during 2001. Growth in all sectors will be slower, but services and construction jobs should continue to expand while manufacturing jobs are expected to decrease by about 1%. Concurring with the labor economist, an economist from the state’s fiscal commission expects the unemployment rate to rise from 4.5% at the end of 2000 to just over 5% by the end of 2001.

Indiana

An economist from a community research institute in northeast Indiana presented the most pessimistic outlook at the roundtable. While the overall economy of Indiana is only undergoing a slowdown, the economist believes that the Fort Wayne area is in the early stages of a recession.

The biggest signs of a recession for the area are increasing layoffs and plant closings. The Fort Wayne Office of Workforce Development reported that, at the end of December 2000, the numbers of new and continued unemployment claims were up 256% from a year ago. The economist noted that, recently, numerous small businesses have run out of money and just “put a padlock on the door,” often without giving employees any prior notice. The biggest drag on the area has been a weak motor vehicle industry, including slowing sales of light, commercial, and recreation vehicles (RVs). RVs are traditionally a discretionary purchase, susceptible to swings in economic activity; during 2000 sales fell 26% nationwide as consumer wealth was eroded by a declining stock market. One small town in the area, where much of the economy is fueled by two RV manufacturers and one RV parts supplier, saw its unemployment rate climb nearly 1 percentage point during 2000. This was in part due to layoffs occurring at those plants, which led to the outright closure of one plant in early 2001.

The economist emphasized that northeast Indiana is in a worse position than the rest of the state, but that the state’s economy as a whole is also slowing. Employment in the Fort Wayne area is expected to decline 1% to 2% over 2001, but employment for the whole state would likely drop by only 0.5% to 1.5%. The state government expects revenues in 2001 to be roughly equal to those in 2000.

Iowa

Like Indiana, Iowa is showing signs of rising unemployment, slower employment growth, and weak state government revenue growth. However, according to the representative from Iowa, an economist with the state government, the state is not in a recession.

The slowdown in Iowa might be similar to those in other District states, but it has been lagging the other states. The economist reported that the number of layoff notices and plant closings in Iowa only began to pick up around the end of 2000; whereas, other District states reported similar conditions during the summer. Some of the layoffs have been spreading from communities where the labor markets could easily absorb the displaced workers to communities where job conditions are not as rosy. Among other signs of a slowdown, the number and dollar value of housing permits fell during 2000, and retail sales in January 2001 were down as well. These conditions contributed to weak revenue growth for the state government. The government forecast for the current fiscal year had been for 3.5% growth in receipts, but through the first half of the fiscal year they were only up 0.2%. The economist noted that in light of this “troublesome” growth figure, some legislators were looking at in-line budget cuts for the current and next fiscal years.

Iowa’s labor markets have been among the tightest in the District, if not the nation, and an overall economic slowdown will likely do little to change that. The economist forecasts that the unemployment rate should rise from 2.5% at the end of 2000 and level off at 3% by mid-year. However, the number of new jobs created will moderate. About 9,100 new jobs should be added during 2001, an increase of 0.6% over 2000. The economist expects a similar growth rate for employment during 2002.

Michigan

Representatives from Michigan universally forecast a slowdown in light vehicle sales, expecting sales during 2001 to range from 15.5 million units to 15.9 million, a decline of 7.6% to 10%. This would leave the state vulnerable to economic weakness during 2001 but, according to an economist from a regional research group and a state government economist, continued expansion in the service economy should cushion the blow to the overall state economy. While one analyst acknowledged being “concerned” about the economy, neither economist forecast a recession for Michigan.

Heading into 2001, manufacturing conditions in Michigan looked bleak. The slowdown in vehicle sales, which began in the second half of 2000, led automakers to cut back production and lay off workers to control inventories. One representative noted that parts suppliers to the auto industry have weathered the slowdown financially better than many analysts expected because they have more flexibility in their employment through use of temporary and nonunion labor. The paper industry, with a presence in west Michigan, is in a “tremendous slowdown,” due in part to overcapacity nationwide. As a result of weak conditions, one economist noted that the purchasing managers index for west Michigan was plunging to “horrible” levels. One bright spot is that the office furniture industry continues to grow, but this sector tends to lag slowdowns in the rest of the economy; and its rate of expansion will probably halve from 9% in 2000 to about 5% in 2001.

Manufacturing employment will probably be the weak spot for Michigan’s labor market going into 2001. The state government economist forecast a 4.5% decline in manufacturing jobs, mostly in motor vehicles and other durable goods industries; but the other economist said that the decline probably will not be that large because many temporary manufacturing workers are counted under business services. However, services employment is forecast to prow a healthy 1.7%, as in 2000, so total wage and salary employment is forecast to fall 0.3% in 2001. The unemployment rate will likely rise from 3.7% at the end of 2000 to 4.8% at the end of 2001. If this labor market forecast holds, personal income growth should be weak.

Wisconsin

A university economist from Wisconsin noted that the economy was in a “choppy” and “scary” transition to a slower rate of growth, but not in a recession, because the economic news is not universally negative; conditions are generally mixed across industries.

Among the negative news cited by the economist, it appears that the manufacturing sector “is in trouble” and layoffs at factories are likely to continue. Wisconsin law requires advance notice for layoffs larger than 50 workers or so, and activity in that office has been significant. Declines in capital expenditures have been bigger than expected. On a positive note, retail hiring remains robust, and labor markets are still tight. Given these mixed conditions, employment should range from being unchanged to expanding a slight 0.3%.

Conclusion

Because the Midwest economy traditionally depends more heavily on cyclical industry sectors then the rest of the country, it also tends to lead the rest of the country in the business cycle. As such, the fact that no participants in the Chicago Fed’s recent Economist Roundtable said they expect their state to enter a recession in the coming year bodes well for the national economic outlook. However, much of the outlook depends on how resistant the rest of the economy is to the sharp decline in manufacturing activity and how well the labor markets absorb the newly laid-off workers from manufacturing plants.

Notes

1 The Midwest is defined here as the states of the Seventh Federal Reserve District—Illinois, Indiana, Iowa, Michigan, and Wisconsin.