Gross State Product Growth and the Midwest Economy Index

In August 2014, the U.S. Bureau of Economic Analysis (BEA) published prototype quarterly estimates of gross state product (GSP). In releasing this quarterly supplement to its existing semiannual releases of annual GSP, the BEA noted that the availability of higher-frequency information on state output should help researchers to better understand national and regional business cycles.

In this blog entry, we take another look at the GSP data for the five states of the Seventh Federal Reserve District to see how they compare with the Midwest Economy Index (MEI) produced by the Chicago Fed.1 We find that the MEI is highly correlated with the new quarterly GSP data; moreover, the MEI remains timelier as an indicator of the Midwest business cycle because it is released on a monthly basis.

In 2011, the Chicago Fed began providing four times a year estimates of annual gross state product growth for each of the five states in the Seventh Federal Reserve District2 as an accompaniment to its MEI release.3 Using the forecasting model underlying these estimates and the BEA’s new quarterly GSP data, we extend our annual projections to include quarterly GSP growth. Below, we present what we’ve forecasted for each District state through the first half of 2014.

The MEI and GSP growth

The MEI is a weighted average of 129 state and regional indicators that measure growth in nonfarm business activity. Two separate index values are constructed, the MEI (providing an absolute value), which captures both national and regional factors driving Midwest economic growth, and the relative MEI (providing a relative value), which presents a picture of the Midwest’s economic conditions relative to the nation’s.

Both indexes are business cycle indicators capturing deviations in growth around a historical trend. MEI values above zero indicate growth above a Midwest historical trend, and values below zero indicate growth below trend. For the relative MEI, a positive value indicates that Midwest growth is further above its trend than would typically be suggested based on the current deviation of national growth from its trend, while a negative value indicates the opposite.

Together, the MEI and relative MEI provide a picture of the Seventh District’s state economies that is closer to being in real time than does the BEA’s GSP data. To see this, consider figure 1, which plots the MEI and the year-over-year gross domestic product (GDP) growth for all five District states combined using the BEA’s annual and quarterly data. The correlation here is quite striking, with the major difference being that the MEI is often released six months to a year (or more) in advance of the quarterly or annual GSP data.4

Figure 1. 7th District GDP growth and the MEI

Forecasting annual and quarterly GSP growth

By exploiting the historical correlation between annual GSP growth in each of the five District states and the MEI, we have been producing quarterly estimates of annual GSP growth since 2011. The statistical model we use to explain the annual growth in GSP for each Seventh District state is shown below.

The model succinctly summarizes the historical relationships between national (real GDP growth), regional (MEI and relative MEI), and state-specific (lagged GSP and state real personal income growth) factors driving each Seventh District state’s annual GSP growth since 1979.

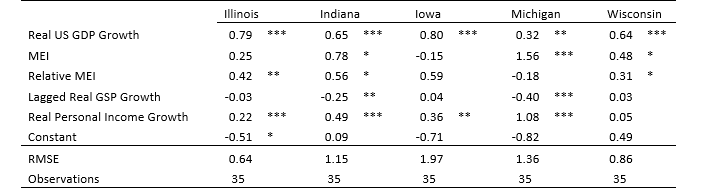

We use a similar model applied to quarterly data to assess how well we can predict growth in the BEA’s new quarterly estimates of GSP. Before we do so, we review the annual GSP growth model. The regression coefficients estimated for our annual model using data through 2013 are listed in table 1. Each coefficient represents the “effect” of an input on GSP growth. For example, a 1% increase in real U.S. GDP growth leads to about a 0.5% increase in GSP growth on average across the Seventh District states (first row of the table).

Table 1. Annual state GSP growth regression model

Source: Authors' calculations based on data from Haver Analytics.

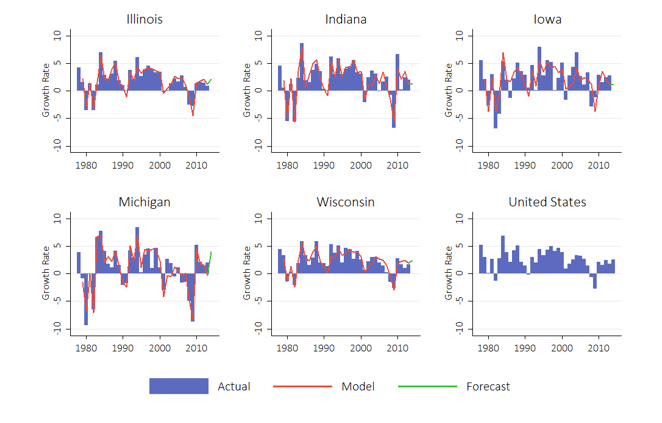

The historical fit of our annual model varies across the five District states, as seen in their root mean-squared errors (RSME) (next to last row of the table). To put these deviations in perspective, we generated figure 2, which plots the actual annual GSP growth for each state, as well as GDP growth for the United States (blue bars), against the fitted values from the regression (red lines). The model does quite well at predicting Illinois’s and Wisconsin’s GSP growth rates, which tend to be less volatile and more closely resemble U.S. GDP growth. Its worst fit is for Iowa’s GSP growth rate, largely because it does a poor job of capturing fluctuations in agricultural conditions.

Figure 2. 7th District GSP growth forecasts (annual)

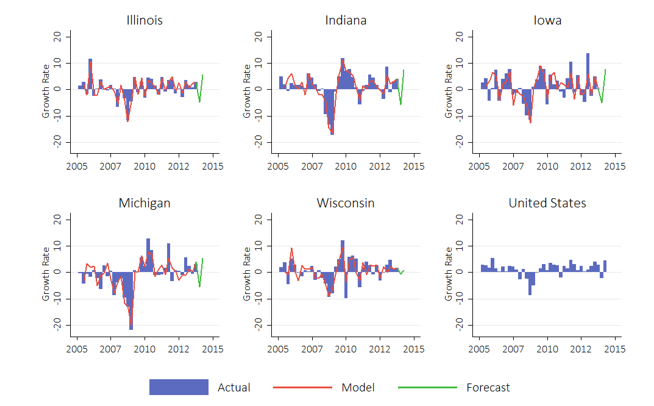

We now extend our analysis using the BEA’s quarterly GSP data. To predict GSP growth for the first and second quarters of 2014, we estimate a “bridge equation” for each District state linking current and previous values of the monthly MEI and relative MEI to its quarterly annualized GSP growth, where the number of monthly lags spans both the current and previous quarters.5 We also include the current and previous quarters’ state real personal income growth and the previous quarter’s annualized GSP growth. We estimate the model on data from 2005 through 2013 and then project forward two quarters.

Figure 3 displays the quarterly regressions’ fitted values (red lines) against actual quarterly annualized GSP growth (blue bars). As our model did with the annual GSP data, it fits quite well for the majority of District states’ GSP growth rates. The green lines in the figure denote the forecasts for the first and second quarters of 2014. We project declines in GSP growth for District states in the first quarter that are largely offset by second quarter growth—consistent with U.S. data. The green lines in figure 2 depict similar annual forecasts for the entirety of 2014.

Figure 3. 7th District GSP growth forecasts (quarterly)

Our 2014 forecasts

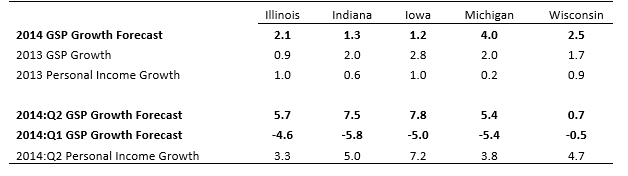

Table 2 shows our complete projections for District states’ 2014 GSP growth rates. Our annual growth projections suggest that Illinois’s growth rate will be closer to the District average in 2014, at around 2%. We project Michigan and Wisconsin to grow at above-average annual rates, while we project below-average growth for Indiana and Iowa. However, our quarterly model projections through the first half of 2014 suggest some downside risk to our annual Michigan and Wisconsin forecasts and upside risk for our annual Indiana and Iowa forecasts.

Table 2. State GSP growth forecasts (percent for annual, annualized percent for quarterly)

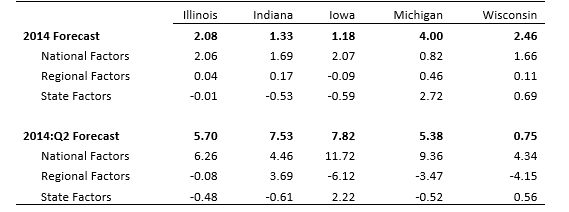

As we’ve seen from tables 1 and 2, each state’s forecast is affected differently by the five inputs to our model. To further illustrate this point, we break down each state’s projected GSP growth rates into the expected contributions from national, regional, and state factors in table 3. National factors represent the effect of national GDP growth on our state GSP growth forecasts. Regional factors capture the roles played by the MEI and relative MEI, while state factors incorporate the effects of state real personal income growth, as well as the idiosyncratic dynamics of each state’s GSP growth.

Table 3. State GDP growth forecast contributions

State and national factors have played a dominant role so far in 2014, but not every District state is projected to share equally in the national second quarter rebound from the slow start to the year. Regional factors have increased in importance over the course of the year; and with both the MEI and relative MEI showing above-trend growth so far in the third quarter, they are likely to continue to do so in the second half of 2014.

As we work to merge our annual and quarterly forecasting models, we will be reporting both annual and quarterly annualized estimates of District states’ GSP growth in conjunction with the MEI. These projections following the third release of national GDP data are available online.

Footnotes

1 This blog entry serves as an update to a previous Chicago Fed Letter examining GSP growth and the MEI, available online.

2 The Seventh District comprises all of Iowa and most of Illinois, Indiana, Michigan, and Wisconsin. The MEI and our GSP forecasts are for the entirety of each state that lies within the District.

3 Our estimates of annual GSP growth are made available following the third release of national gross domestic product (GDP) data for each quarter online.

4 The 2014 release schedule for the MEI and the quarterly GSP growth forecasts are available online.

5 A similar model linking quarterly annualized U.S. GDP growth and the Chicago Fed National Activity Index is described in an article available online.