The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

An April 1989 survey of the futures and options trading practices of 127 commercial banks indicates substantial increases in trading of foreign-currency options since 1986. Overall, trading by banks in these financial instruments increased at an annual rate of about 80%. Exchange-traded foreign-currency options on futures contracts, the newest form of currency option, increased by about 40% annually. Prior to 1980 hedging in foreign-currency markets was limited to contracts traded in the forward and futures markets. These markets were used, in the main, by large corporations and dealers. There was little room for smaller players.

The development of markets that trade options on spot or futures contracts provides alternative hedging instruments. These newer instruments are valuable because they allow a flexible risk management that was formerly available only through over-the-counter transactions. They allow a style of risk management we might call "homemade hedging." Today, for example, daily trades in options on foreign-exchange futures contracts average 37,500 contracts. These contracts have a total face value of $2.8 billion.

This Letter contrasts hedging with futures and hedging with options on futures and identifies some advantages of options on futures. Chief among these advantages is the greater flexibility afforded to risk managers. Additionally, options on futures frequently enable small businesses to manage their exposure to foreign-exchange risk with fewer and smaller cash outlays than may be required in the forward or futures markets.

The hedger’s problem

Firms hedge to control exposure to some risk. The potential for damage when dogs are allowed in the yard is suggested in the title of this Letter. To control this particular exposure we might use a hedge. Financial obligations also create exposure to risk. For example, foreign-currency invoices or receipts expose a firm to changes in the value of that currency. Adverse changes in the price of the currency can mean that receipts are less valuable or expenditures more costly than originally planned.

These two financial situations can be illustrated in dollar terms. First, when foreign-currency receipts are converted to dollars after a rise in the value of the dollar, the exchange produces fewer dollars. Second, when foreign-currency expenditures must be made after a fall in the value of the dollar, the dollar cost of the expenditures is greater than planned. In either case, operating budgets are squeezed and managers are forced to redirect resources. Just as with managers of yards, financial managers may seek to control these exposures with a hedge.

Futures and options on futures

Futures and options on futures are derivative assets; that is, their values are derived from underlying asset values. Futures derive their value from the underlying currency, and options on currency futures derive their value from the underlying futures contracts, which in turn derive their value from the underlying currency itself.

In the traditional futures contract, if the price of deutschemarks rises by $0.01 we generally expect the near-to-delivery futures contract on deutschemarks (DM) to rise by the same amount. Because of this near one-to-one correspondence, a manager holding 250,000 DM (a long-cash position) can hedge by selling (going short) two futures contracts—each contract for 125,000 DM (a standard futures contract for DM). Once this correspondence is established it becomes clear that a planned expenditure of deutschemarks (a short-cash position) can be hedged by buying (going long) futures contracts. In both cases, the only adjustment needed is the number of futures contracts.

When the value of the underlying asset changes, the value of the futures contract changes also. The unit used to measure value changes in the derivative products—whether futures or options on futures—is called delta. In the example above the delta is one because a $1 change in the value of the underlying asset—in this case 125,000 DM—leads to a $1 change in the value of the futures contract. As a result, 100% of the foreign-exchange risk was covered by the short futures contract. If we hedged a position of 250,000 DM with one futures contract requiring delivery of 125,000 DM, only about 50% of the foreign-exchange risk would be covered.

The relationship depends on several considerations, but when the cash asset being examined is very similar to the asset delivered in the futures contract, the result is generally a delta of one. The delta of a futures contract is based on observation of past changes: Past changes in the cash market are related to past changes in the futures market.

Option deltas

Options on futures contracts also have deltas. These deltas relate the price changes of options to those of the underlying asset. This makes sense when we consider how these options are related to futures contracts. A call option provides the owner with the right to buy the underlying asset at a price and time established in the contract. The price is termed a strike price and the time is its expiration date. Thus, calls on futures contracts are rights to buy futures contracts at fixed strike prices on or by their contract expiration dates.

Options on futures are categorized according to their strike prices. An option is “in-the-money” when its strike price is less than the future’s price; it is “at-the-money” when the strike price equals the future’s price. When an option is “out-of-the-money,” its strike price exceeds the future’s price.

As noted earlier, values of options change with the underlying asset. The underlying asset is a futures contract but then the value of that contract changes with the value of the cash asset. So when the deutschemark rises by $0.01, the price of a call option on the nearby (soon-to-mature) deutschemark futures contract, having a strike price equal to the future’s price (“at-the-money”), will rise by about one-half that amount, $0.005. In other words, its delta is one-half. This is because, in general, the change in value of an at-the-money option is half the change in the value of the underlying asset.

This means our long deutschemark position could be hedged by selling a call option on the futures contract. Since the delta of this call option is one-half, 50% of the risk of 125,000 DM is covered. We can cover more of the foreign-exchange risk by selling two options having deltas of one-half each to cover 100% of the risk of l25,000 DM or selling four options to cover 100% of the risk of 250,000 DM. In other words, deltas are cumulative—they can be added together. Each delta of one covers a cash market position that is equal to the size of the futures contract.

With options on futures, the delta of an option is largely determined by the difference between the strike price and the current cash price. If the current cash price greatly exceeds the strike price, changes in the price of the option should closely match changes in the cash price; that is, the option delta is close to one. As the likelihood of exercising the option declines, the option becomes a less close substitute for the futures and the delta declines.

This is an important point. To keep transactions costs low, hedging should be done with as few options as possible. Hedging with options will be most cost-effective when the options are in-the-money—when, that is, the futures price exceeds the strike price of the option.

Option deltas change as the expiration date nears. This means that an options-hedged position may require recomputing deltas and, if the position risk becomes too great, changing the position by buying or selling options.

Advantages

Hedging with options on futures has three advantages. First, risk can be significantly reduced. Second, a trader can take positions smaller than standard futures contracts. Third, options on futures provide more flexibility than futures.

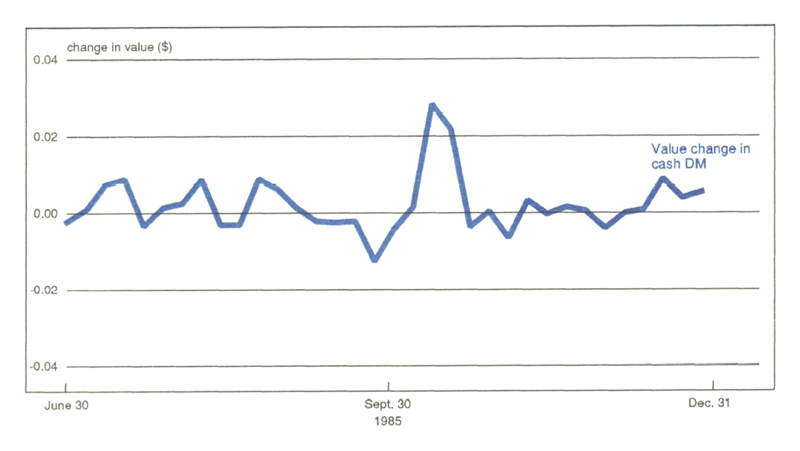

To illustrate the reduction in risk with options on futures, I first determined price changes of the deutschemark for five-day holding periods during the latter half of 1985. The amplitude of the price changes indicates substantial cash-market risk (see figure 1). Price changes greater than $0.003 occurred 17 times, nearly 37% of the periods examined. For a cash-market position of 250,000 DM this represents a change in value exceeding $750 each week.

1. When the DM is jumpy…

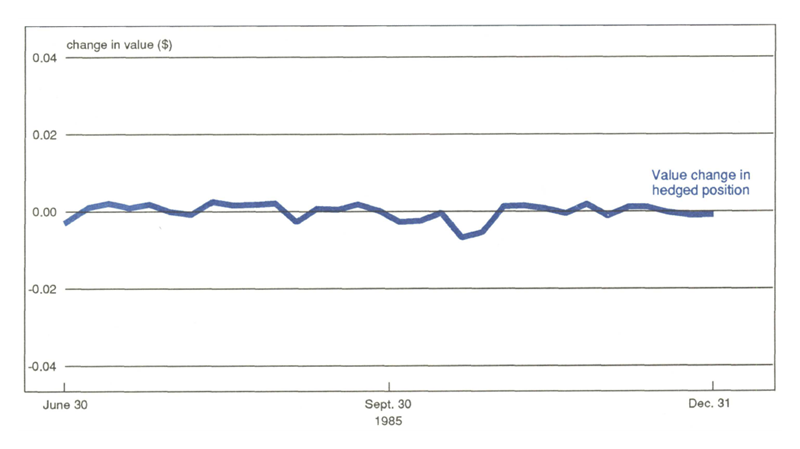

To determine the effectiveness of hedging with options on futures, I calculated delta for near-the-money calls on the deutschemark and constructed hedges during the same time period. Figure 2 illustrates daily changes in the value of these hedged positions.

2. …Options can dampen the changes

Comparing the two graphs, note the reduction in the amplitude of the hedged position (figure 2) in comparison to figure l. Risk has been substantially reduced—now only one day experienced changes of $0.003 or greater. This difference illustrates the reduction in risk obtained. Measured in percentage terms, risk was reduced on average by 90.5% for these five-day holding periods. This was only slightly less than the risk reduction achieved when futures were used for the same holding periods. In general, the risk reduction achieved when hedging with options on futures compares very favorably with futures hedging.

A second advantage is that traders can take positions smaller than the standard futures contract. For example, selling a call with a delta of one-half will generally hedge a position of 60,000 DM more effectively than will selling a futures contract delivering 125,000 DM. Even smaller positions can be hedged using options with smaller deltas.

Consider a hypothetical US exporter of chopsticks. A shipment of chopsticks is scheduled for delivery in one month with payment of, say, 1,420,000 yen on delivery. At 142 yen per US dollar, the shipment brings $10,000, for a presumed net profit of $1000. A fall in the cost of the yen, say to 145 yen per dollar, cuts net profit to $793.10, a loss of 20.7% in net profit. The standard futures contract is 12.5 million yen, far too large to be useful in this case. Therefore, the exporter sells a call option on the yen futures contract to cover the possibility of loss. The option contract produces a gain when the yen falls which offsets the loss on the chopstick sale.

Third, considerably more flexibility is available when options on futures are added to the hedging menu. Managers using out-of-the-money calls or puts can cap their exposures. These sorts of hedges cannot be easily constructed for small positions with futures contracts. For example, suppose a banker is committed to selling 250,000 DM in 30 days. At the present range of exchange rates, the risk is acceptable. If rates rise by, say, $0.02, the risk of further increases is regarded as unacceptable. Buying two call options with exercise prices $0.02 above the current exchange rate results in the following: Exposure to price changes is immediately reduced (but by less than 100%) and, if exchange rates do rise, the amount of coverage is increased. This is because the delta rises as the price of the option rises. In effect, the position becomes more effectively hedged as exchange rates approach the unacceptable level. The cost is the price of the two options.

In summary

Hedges protect yards from dogs and businesses from financial exposure. Hedges can be constructed using futures or forward contracts. Alternatively, a relatively new instrument—options on futures—can be used by hedgers. In particular, as trade and financial dealings become increasingly global in scope, options on futures can provide an effective hedge against foreign currency risk. The key advantages of options on futures over futures are two. First, options on futures enable small businesses to hedge more effectively. Second, options on futures provide greater flexibility when hedging by allowing the hedgers to cap their exposure. The improved control over foreign-exchange exposure helps to explain the rapid growth of these options as shown by the considerable increase in their utilization by banks. Although this Letter only addresses options on currency futures, options on futures can also be used to hedge risks arising from other sorts of obligations or commodities.

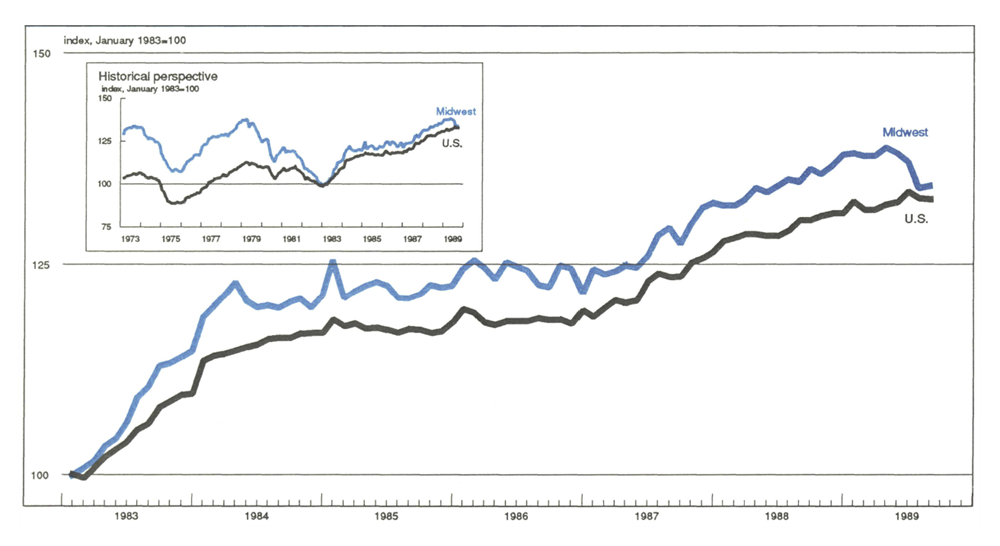

MMI—Midwest Manufacturing Index: Current expansion

Midwest manufacturing activity peaked in April, and in August stood about 3% below that level. This regional weakness, however, may be overstated. Two industries (food processing and chemicals), which accounted for much of the decline, were coming off very high levels at the beginning of the year and appear now to be settling back to longer-term trend growth. Also, transportation equipment continues to be hampered by production cutbacks in Michigan.

Midwest manufacturing activity edged upward 0.2% in August from July, largely on the strength of durable-goods production. In contrast, the U.S. index declined in August for the third straight month.