The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

The new administration may not find a “kinder and gentler” financial sector in 1989, but it is likely to find a prosperous goods-producing sector. Financial markets—burdened by large federal debt financing needs and dependent on foreign capital inflows—will be vulnerable to swings in exchange rates and bond prices. But most manufacturers should enjoy further expansion in 1989, supported by rising investment, favorable exchange rates, and expanding exports. For the industrial Midwest, the anticipated good fortune of manufacturers is welcome news.

This encouragingly optimistic outlook was the consensus view of the second annual Economic Outlook Symposium sponsored by the Federal Reserve Bank of Chicago. The Symposium, held on December 7, 1988, brought together business economists from around the Midwest to discuss issues that will be shaping the national economy in 1989. Participants were economists and analysts from major industrial firms, financial institutions, and other organizations in the Midwest. Their comments offered an overview of a broad cross-section of business activity in the Midwest. Of the 34 participants, 26 provided annual and quarterly projections through 1989 for several key measures of the national economy.

Most expected the U.S. economy to complete its seventh year of expansion in 1989. However, the group’s optimism was tempered by concerns about weakness in some sectors of the economy, the risk of higher inflation, and continued large federal deficits. This Chicago Fed Letter looks at the December discussion of the economic outlook for 1989 from a Midwestern perspective.

A seventh year of expansion

The relative optimism of the group is apparent in its median forecast of 2.3% growth in inflation-adjusted Gross National Product (real GNP) on a fourth-quarter-over-fourth-quarter (4Q/4Q) basis in 1989, as shown in figure 1. Real GNP growth of 2.3% in 1989 would represent an impressive achievement, given the longevity of the current expansion. Although below the 3.9% pace set in 1988, this growth would extend the second longest U.S. expansion on record (the longest was the 1961-69 expansion). The narrow spread from 1.9% to 2.6% of the interquartile range (a measure that excludes the highest and lowest one-fourth of the forecasts) suggests considerable agreement about the sustainability of the expansion.

1. GNP growth forecast: Moderate expansion

This GNP growth was expected to be attained with inflation little changed from last year’s pace. Specifically, the GNP implicit price deflator was expected to rise 4.1% in 1989 (4Q/4Q), up only slightly from 3.9% in 1988. This inflation forecast as well as the growth in GNP, are comfortably within the range of monetary policymakers’ expectations, as described in the most recent semiannual congressional testimony on the subject last July. At that time, Alan Greenspan, chairman of the Federal Reserve Board, stated that the Federal Open Market Committee (FOMC) expected real GNP in 1989 to grow in the range of 2% to 2.5%, and the GNP deflator to rise in the range of 3% to 4.5%.

These FOMC forecasts are closely watched by business and investors. If price increases appear to be exceeding the Fed’s projected range, these people expect monetary policy to tighten, threatening the current economic expansion. However, the consensus 1989 forecast at the December meeting was well within both the GNP and inflation ranges cited by the FOMC.

Cautionary notes

Much of the strength in real GNP growth is concentrated in the first quarter and can largely be attributed to drought effects. Government statisticians expect 2.8 percentage points of the first quarter’s reported growth rate to result from a recovery in seasonally adjusted agricultural production, following losses brought on by last summer’s drought.1 Removing 2.8 percentage points from first quarter 1989 GNP growth would reduce the consensus forecast for the quarter to a 0.7% growth rate. The consensus forecast shows 2% growth in each quarter thereafter. With the drought adjustment, then, 1989 GNP growth would be somewhat below the lower bound of the FOMC’s range.

There is, of course, a risk that real GNP growth could fall below the consensus forecast. The fact that the consensus is flat at 2% for the remaining three consecutive quarters means that half of the forecasts for each quarter are at or below the lower bound of the range cited by the FOMC. One forecaster anticipated a recession in the second half of 1989, while another expected a recession to begin in 1990. A recession or even sluggish economic growth would raise unemployment and, along with it, political pressure to stimulate the economy.

The forecast for 1989 does include declines or weak growth in some sectors. Residential fixed investment was expected to be only about even with 1988 and consumer spending growth was forecast to slow in 1989 to about 2% from about 3% in the previous year. Those forecasters who were explicit about their expectations for the various components of consumer spending foresaw lower outlays for durable goods. For example, motor vehicle unit sales (mainly to consumers) were expected to be 2% lower next year by one forecaster, and down 5% or more by another, which implies lower auto production and less demand for steel and other inputs. Major appliance sales were also expected to decline 2% to 4% in 1989, which reflects the slowing in new housing construction and the end of a bulge of appliance replacement demand during the mid-1980s.

Reinvesting in America

Investment spending, vital to improve America’s competitiveness and to enhance the economy’s long-run growth potential, is expected to rise 3% during the four quarters of 1989. While less sharp than the 8% increase in 1988, investment growth is clearly the bright spot in the forecast. Key sources of this growth, cited in the discussion, included the need to expand capacity to meet growing domestic and foreign demand by some industries and the end of downsizing by others.

Investment growth was expected to be particularly strong in chemicals, petrochemicals, and paper, which have been pressing full capacity. Plant and equipment spending growth in these industries should be well above the rate of increase in total capital spending. Also likely to add to capacity are such diverse industries as glass, appliances, food processing, airlines, printing, tires, and electrical equipment.

The economists projected that export demand, driven by the lower dollar and stronger foreign economies, would continue to encourage investment spending among machinery and equipment producers in 1989. Investment will be enhanced by the shifting of procurement of components and finished products from foreign to domestic suppliers. The establishment of U.S. plants by foreign-based producers in numerous industries will also add to investment. A substantial portion of this latter investment is occurring in the Midwest.

Among industries that had been cutting capacity by closing old plants in the face of falling demand are mining, steel, and machinery. Economists familiar with these industries reported that recovery was well underway. Mining industries generally have been reinvesting heavily, as commodity prices have recovered. The steel industry also has a large investment program underway to improve efficiency and quality, aimed at meeting tougher specifications of auto manufacturers and other customers and at competing with imports. Machinery used in lumbering and pulpwood production (for the paper industry) is in very strong demand, both for replacement and for new capacity. Adverse effects of the decline in housing construction on lumber demand are being offset by higher exports. A maker of farm machinery thinks a 15% to 20% rise in farm machinery sales in 1989 is achievable, because farm programs will permit a large increase in acreage.

But even investment growth has its limits. An economist for a high-tech manufacturer cited leading indicators for some sectors of the electrical equipment industry that were turning downward in 1988. These indicators, based on orders and shipments data, suggest that these sectors could weaken in 1989.

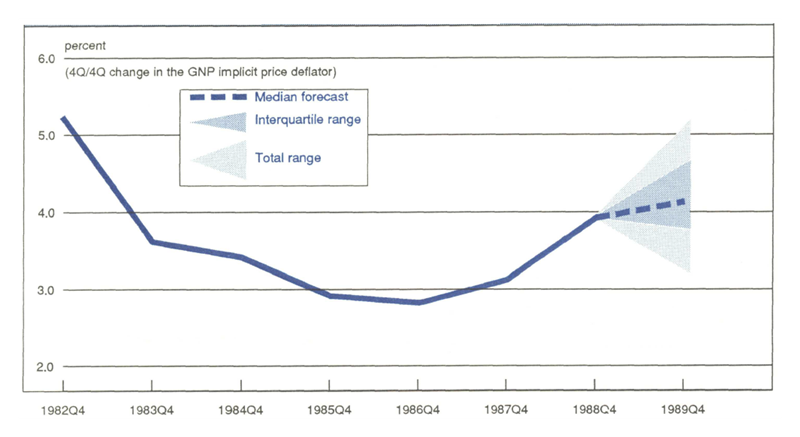

Inflation—Is there a braking point?

The consensus forecast was for relatively steady inflation in 1989, no higher than 4.3% and never lower than 3.9% in any of the four quarters (see figure 2). In fact, a number of participants reported improvements in price trends in their industries. One industrial firm’s purchasing staff described their markets as tight during much of 1988 but expected those markets to be less tight in 1989. Smaller price increases in 1989 were expected for various industrial materials. The completion of capacity expansion projects in some industries—for example, industrial-grade paper—should ease pressures on materials prices in 1989.

2. Inflation forecast: Moderate, with some upside risk

Hopes for a recession-free economy in 1989 were clouded for some forecasters, however, by concerns that more rapid inflation might induce policymakers to apply the brakes to the expansion. The pattern of inflation forecasts suggests that the risk of significantly higher inflation than the median forecast is somewhat greater than the likelihood of substantially lower inflation. The interquartile range extends from 3.8% to 4.6%.

The highest fourth of the forecasts clusters around 5%, above the upper bound of the FOMC’s range. Price increases have already been substantial for some commodities, and these are being passed through to other sectors. Product and labor markets generally have also tightened over the last year. Clearly, a number of forecasters at the meeting expected further heating up of inflation, which would increase the likelihood of further monetary policy tightening.

Will they or won’t they tighten?

About half of the forecasters indicated that their outlook assumed restrictive monetary policy. Further efforts to slow economic activity—in order to reduce the inflation risk or cut the trade deficit—could push the economy toward recession, according to some in the group.

On the fiscal side, the forecasters expected deficit reductions to be difficult to achieve in view of the Administration’s self-imposed limit on new taxes and the cost of various spending initiatives competing for available funds. A former acting director of the Congressional Budget Office attending the meeting cited several major areas within the federal budget facing demands for expanded spending. These included cleaning up nuclear weapons plants; dealing with the thrift industry crisis; providing for the health care needs of those without health insurance; and addressing the long-term nursing care needs of elderly persons without adequate resources. If spending for these and other programs is expanded, Congress’ own targets for deficit reduction (under the Gramm-Rudman-Hollings law) will be pushed even further out of reach, unless offset by spending decreases in other programs or revenue increases.

The difficulty in forecasting policy was brought sharply into focus by a financial economist who presented alternative monetary and fiscal scenarios, using a traditional demand-driven macroeconomic model. He found, among other things, that restrictive fiscal policy, even if offset by easier monetary policy, could depress GNP growth without much lowering of inflation, at least in 1989. Results would vary depending on the type of model used and on the composition of policy changes assumed in generating the scenarios. But the point is simply that each choice carries a cost that must be evaluated.

Seeking a soft landing

Slowing of aggregate economic growth into line with increases in productive capacity enhances the likelihood that economic expansion can be prolonged without the acceleration of prices. Reaching such a long-term growth path without overshooting is sometimes referred to as a “soft landing.”

The relatively favorable 1989 economy portrayed by the median forecast—with real GNP growth at a sustainable pace, little further acceleration of prices, and continued expansion of the nation’s productive capacity—could be just such a soft landing.

MMI—Midwest Manufacturing Index

Manufacturing activity in the nation posted solid gains in November, up 0.5% from October. Business equipment-related industries again led the expansion. Petroleum and electrical equipment were among the few industries that experienced declines. The dip in electrical equipment, which followed a very strong advance in October, was due to lower production of home appliances.

The expansion of manufacturing activity in the Midwest was particularly strong in November, up 0.8% over October’s pace. The key sources of the gain were food processing, chemicals, and fabricated metals industries. However, eight of the 17 industries in the MMI were down slightly from October levels, including petroleum and electrical equipment.

Note

1 See October 1988 Survey of Current Business, U.S. Department of Commerce, Bureau of Economic Analysis.